Diamonds or Dust, Coal Under Pressure

Coal in the US is benefiting from both targeted and indirect policy decisions, somewhat arresting its 15-year decline. We look at operations within and outside markets, a global view, and a significant emissions uptick in 2025.

From emergency orders to the war in Iran, the Trump Administration has kept coal in the headlines, but even before the 202(c) orders started rolling in, coal generation’s decline in America had slowed.

Volatile natural gas prices, load growth, rising capacity payments, slowdowns across supply chain and planning processes, and a rollback of environmental regulations have all converged to provide purchase for America’s remaining coal fleet. Not only to extend survival, but even increase generation across the country.

What We're Covering

- Coal's Decline

- An Administrative Reprieve

- What Did Retire?

- Coal Transportation

- Market-Specific Views

- A Global Look

- Emission Controls

- What Comes Next

We'll be at ERCOT's Innovation Summit next week and the PJM Annual Meeting in May, feel free to reach out if you want to connect in person at either event.

Pipeline Pressure

Coal has a long history in the US, and remains a dominant player in the energy sector across the world. While renewables, batteries, and natural gas comprise nearly the entirety of the national interconnection queue, a large portion of the US electricity sector still relies on coal for grid stability, particularly during events that challenge generation from natural gas and renewables.

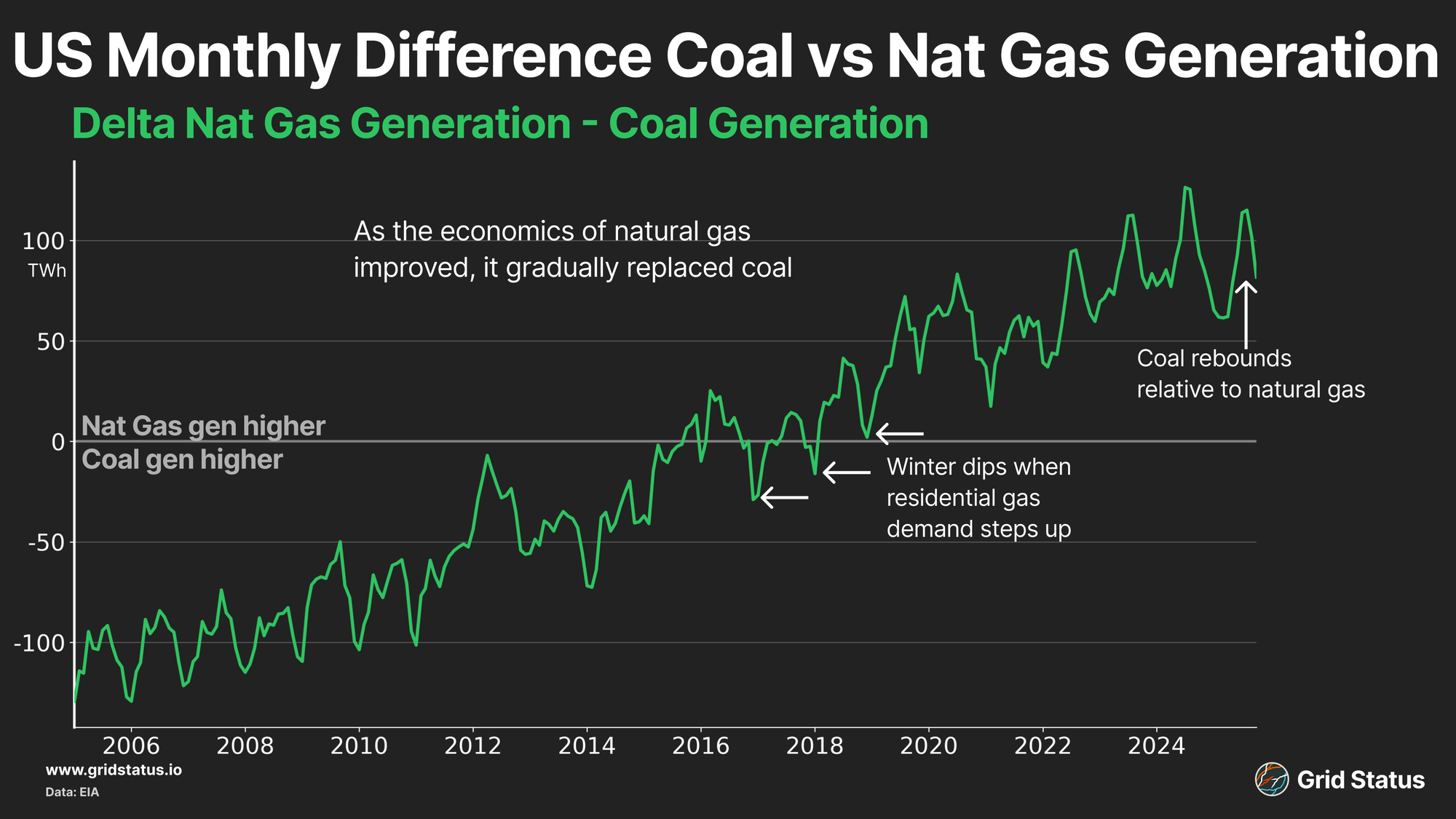

Many were quick to blame coal’s decline on the push to bring wind and solar online, but the main driver was another fossil fuel, natural gas. Following the fracked shale revolution in 2008, and the year Tony Stark became Iron Man, natural gas production boomed and prices, while not immune to volatility, cratered. This fueled the buildout of combined cycle plants, which were substantially more efficient and flexible than traditional coal-fired steam turbines. Falling energy and capacity prices made coal increasingly uneconomic, which, paired with plant aging, limited flexibility, rising maintenance costs, and stricter environmental standards made retirement the typical choice.

In 2025, this trend took a new turn, under the wing of energy “dominance”. Don’t be afraid of getting dirty, we’re diving in to see what’s beneath the surface.

An Inverse Irish Goodbye

The Trump administration’s slogan has been Energy Dominance, but this ethos only extends to certain technologies. If you’re big, loud, and burn you’re getting support, missing any one of the trifecta and you’ll have a much harder road from the federal government. Coal represents all three attributes to a T. Energy Dominance hasn’t just been executive order rhetoric, but manifested in significant and ongoing extension orders for coal plants that had previously planned retirement.

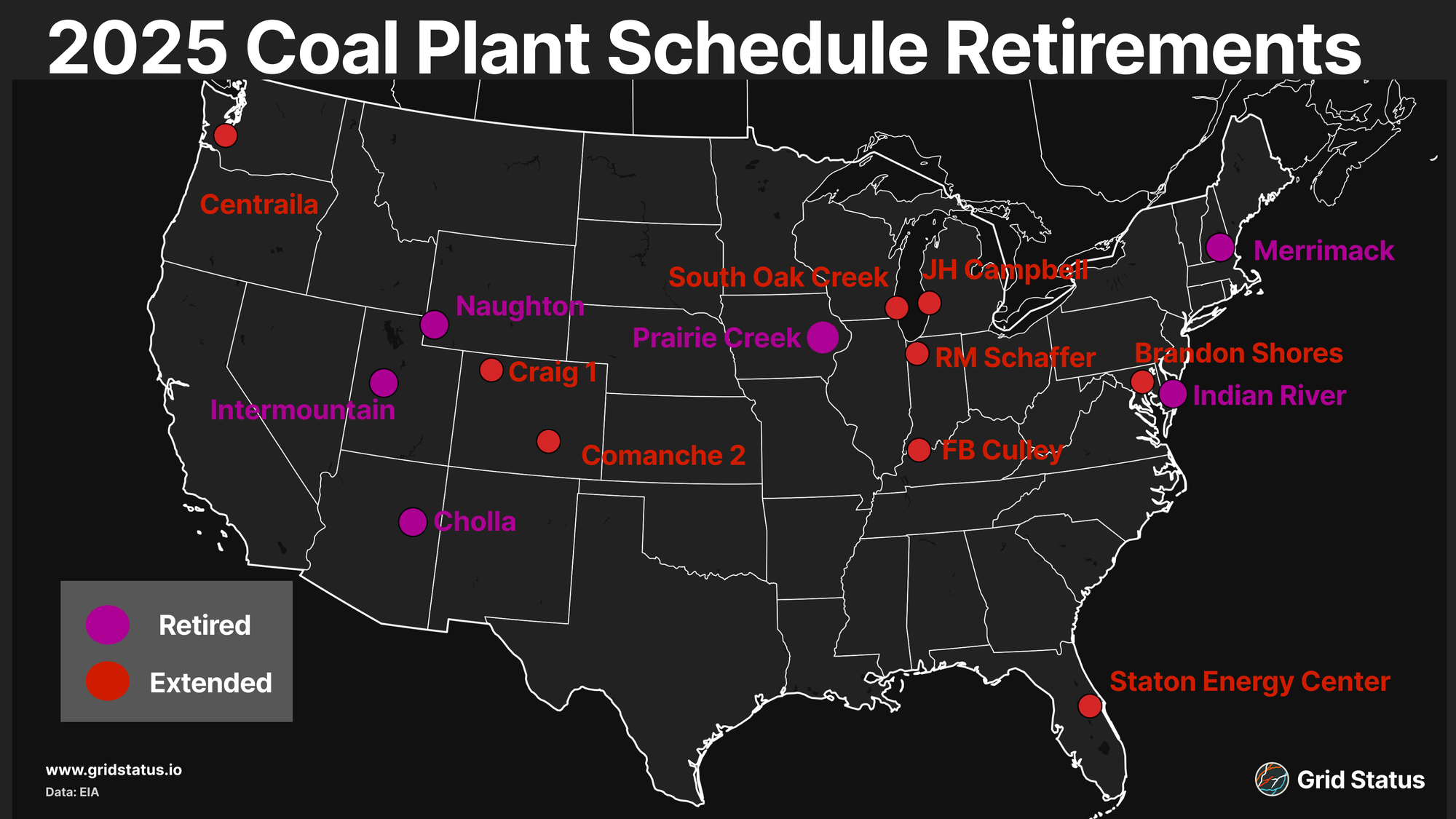

At the beginning of 2025, the EIA reported nine GW of annual retirements across 12 different plants. By New Year’s Eve, only three GW had officially retired. Six coal plants did pulverize their final tons in 2025: Indian River in Delaware at 445 MW, Prairie Creek in Iowa at 15 MW, Cholla in Arizona at 425 MW, Intermountain Power Project in Utah at 1640 MW, Naughton in Wyoming at 775 MW, and Merrimack at 400 MW in New Hampshire (which technically was a deactivation so this unit does not show up as an official retirement in the EIA data). Ultimately, however, more plants (and capacity) remained online.

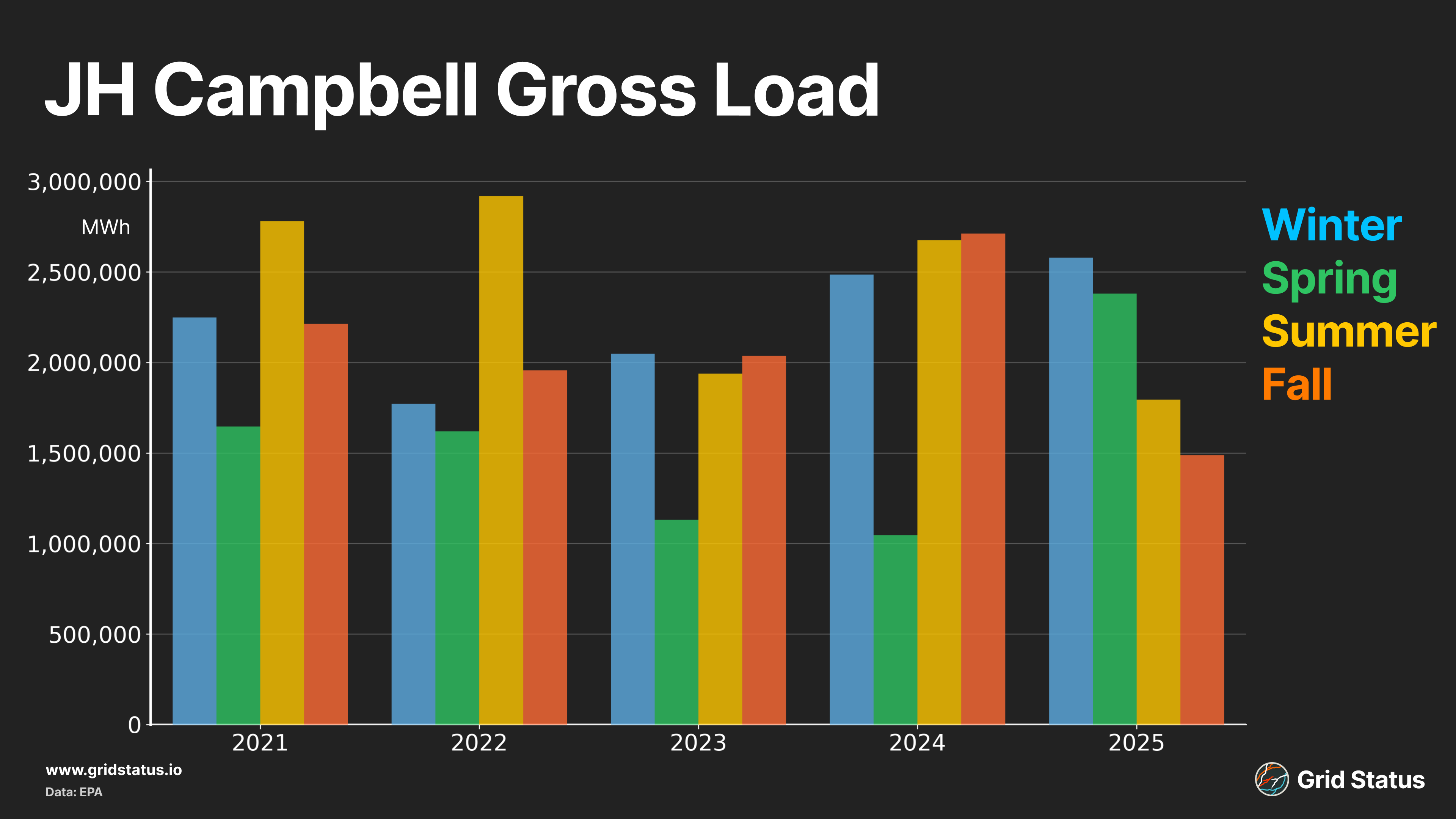

One of the extended units that has seen the most attention is MISO’s JH Campbell, a 3-unit,1,560 MW plant located on the eastern shore of Lake Michigan. Consumers Energy, the plant's owner and operator, had initially set the relatively new plant's deactivation date for May 31, 2025.

In the years preceding the planned deactivation, plant output had fallen, yet followed a typical seasonal pattern. Summer and winter both saw the highest plant output, particularly during 2022 when high gas prices pushed coal back towards economic parity. Plant output would fall off in the spring and fall, when mild load limited the need for this unit. With retirement on the horizon, seasonal patterns took a backseat, and last spring saw a major increase in plant output as operators sought to burn through remaining supplies before deactivation, a dead coal bounce.

While plant operators expected to shut the units down ahead of their scheduled lifetime, the plant was kept online via emergency powers granted to the Secretary of Energy under Section 202(c) of the Federal Power Act. Under this power, the DoE ordered the plant to remain online for 90 days, an order which has required renewal every three months.

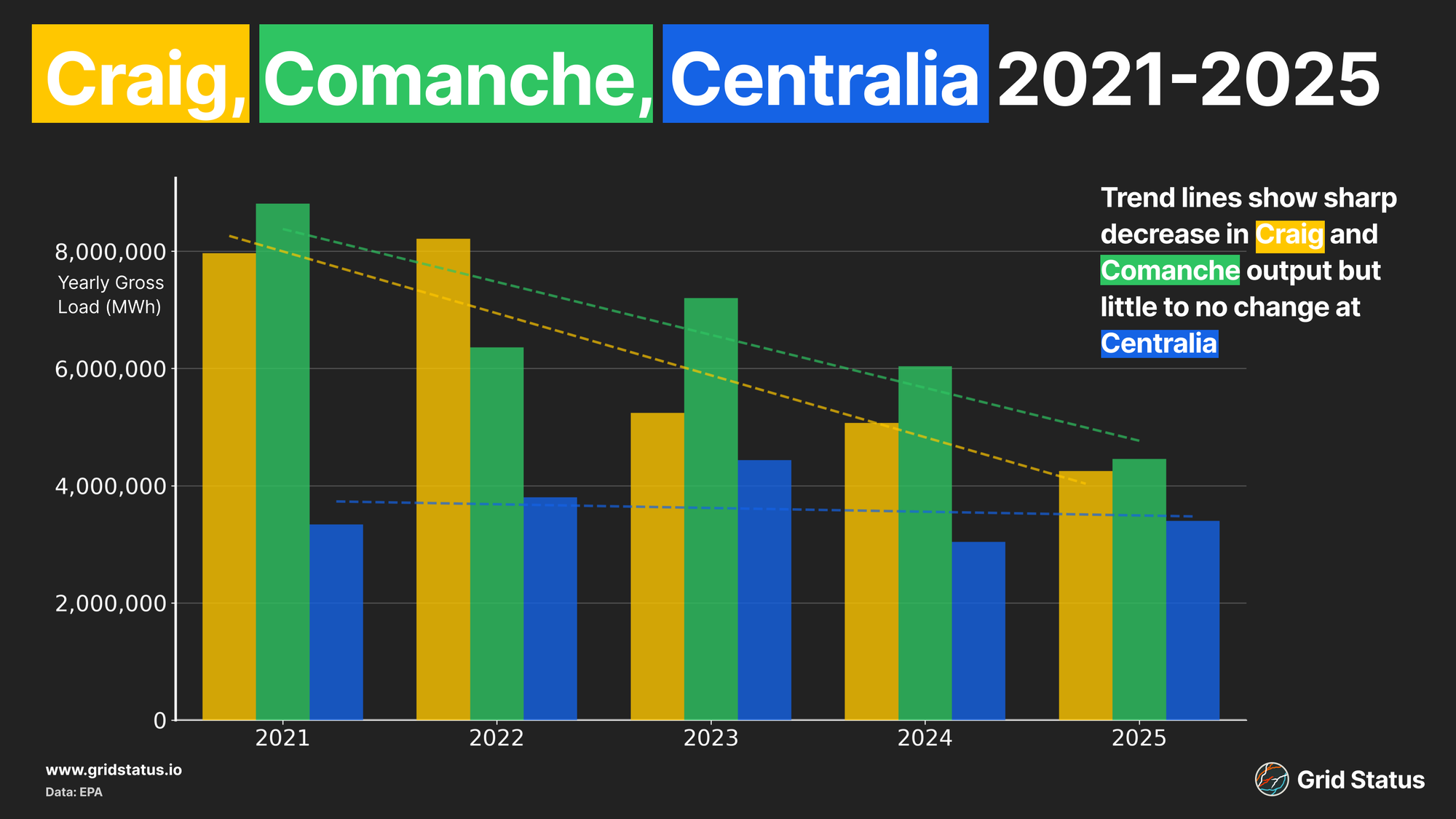

Section 202(c) orders were not just issued for plants that were fully expected to retire. Two coal units in Colorado, Craig 1 and Comanche 2, were kept online in 2025, though under different circumstances. Comanche 2 was extended for reliability reasons as the plant's other unit, Comanche 3, is currently undergoing extensive repair. These repairs, which are expected to take over a year, left PSCO with limited dispatchable power during the peak seasons.

The extended outage at Comanche 3 points to a wider issue at many plants, one that is also impacting Craig 1. As plants age, maintenance, as well as new costs, like scrubbers to meet enhanced emissions standards, cut into operating expenditures. While rising power and capacity prices have made existing assets more profitable in recent years, these costs come after tight margins at many units over the 2010s and early 2020s. This is the case at Craig 1 as well, which has seen generation drop over the years and suffers from deferred maintenance. Plant operators argued that they had built up sufficient wind and solar resources that made the plant unnecessary, filing a petition against the DoE making that exact argument. Craig also has units 2 & 3 that are currently in better condition and continue to run and support the stack.

Coal generation at Craig and Comanche has decreased steadily over the 2020s, with gross output declining to half of what it was 4 years ago. The plan is to replace Comanche coal with solar and a battery connected to the same transmission network. Buildout of the solar portion of this project has already started, but the battery portion has seen delays in permitting and has yet to start construction.

One of the most questionable 202(c) extensions is of the Centralia plant in Washington. The 735 MW unit, owned by TransAlta, was scheduled to retire at the end of 2025, marking the end of coal-fired generation in the state. That was up until the DoE stepped in, forcing the plant to remain online.

When this announcement was made, it was a bit confusing whether this unit had run since 2022, as coal gen disappeared from PACW’s fuel mix according to reporting from the EIA. Looking at the data from the EPA, it appears this plant has continued to run. TransAlta owns the plant and has been selling the power via a long-term contract with Puget Sound Energy. EPA data shows the highest burn during the fall season when flows from the Desert Southwest are strapped and reservoir levels for hydro generation are at their lowest.

TransAlta has also signed a contract with Puget Sound Energy to convert Unit 1 from coal to natural gas, with a rated capacity of 700 MW. Unit 2 was given the coal operation extension, and given the recent history we wanted to explore its continued feasibility. A recent satellite image confirmed some onsite coal, although the pile is quite small.

Most of the coal pile storage area has been scraped clean, and if you look closely, you can even see what looks like bare earth.

Centralia was just extended again, into the summer, despite running so little so far in 2026 that its output would round down to zero.

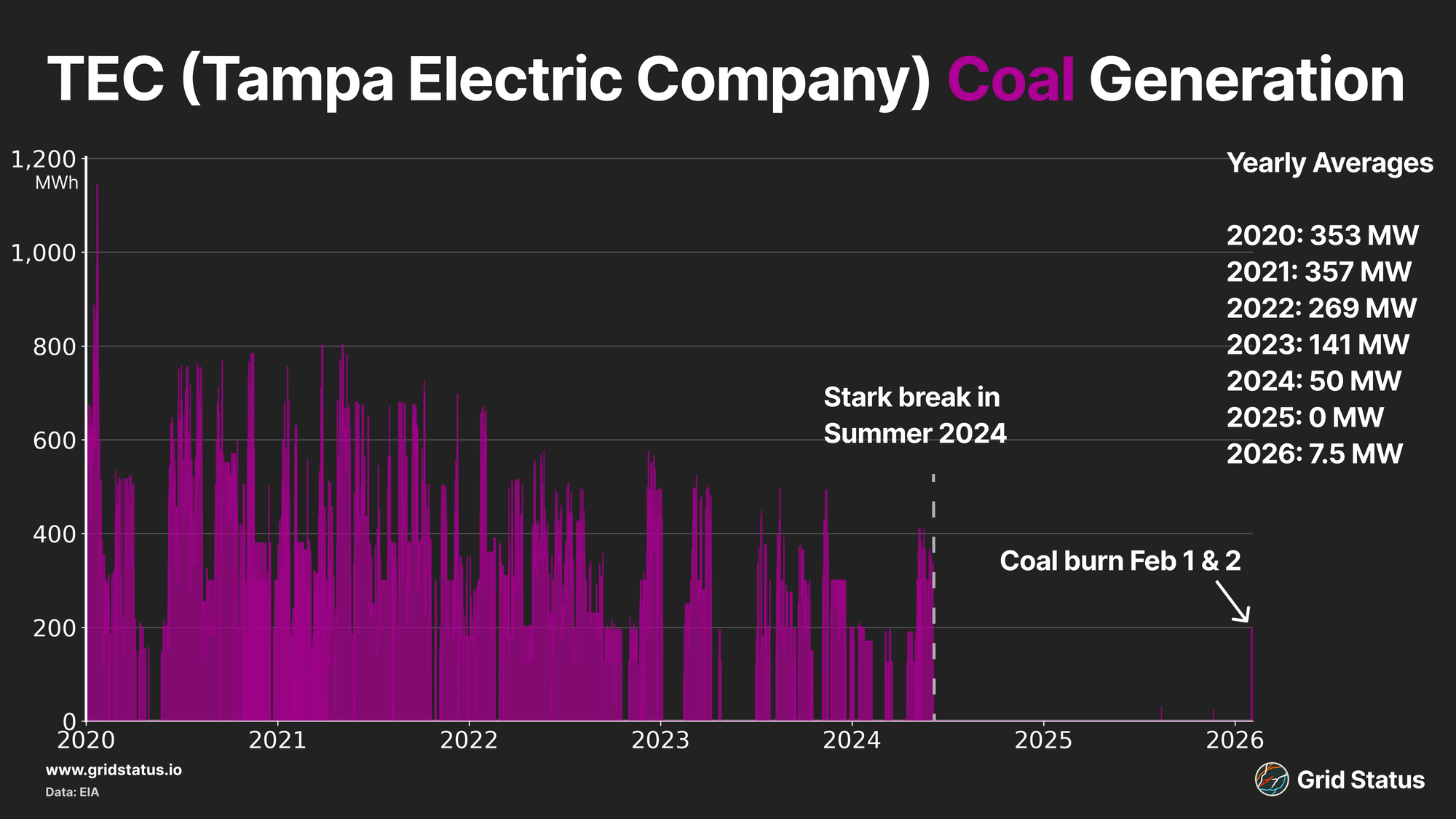

Winter Storm Fern recently showed that the return of long-idle coal plants is not impossible. Big Bend Power Station, owned and operated by Tampa Electric Company, ran for the first time since summer 2024 during a cold snap in the Sunshine State.

TEC had converted most of the units of the plant to natural gas, but a single coal unit remains. Cold weather pushed into the state, leading to a combination of natural gas constraints. Load increased dramatically as electric heating impacts were felt and TEC turned to coal at Big Bend, which had maintained a significant pile, to help supply the stack despite sitting idle for 1.5 years. The last coal delivered was in December 2024, 2025 this plant only saw 184.4k tons delivered which was half the amount delivered in 2023.

While coal plants are not immune to adverse weather events, solid fuel stored on site can be beneficial in specific circumstances, particularly when the just-in-time natural gas system is juggling freeze-offs with maintaining linepack to support distribution systems.

However, a plant that doesn’t run isn’t free, and intermittent thermal plants in particular tend to have costly O&M cycles.

3 Very Different Gigawatts

While some plants were kept from retirement, and others returned from hiatus, a handful mentioned above retired in 2025. Near the beginning of the year we covered the retirement of Indian River on the Delmarva peninsula after an early end to its reliability must run (RMR) agreement. Since then, a few more have exited the stack.

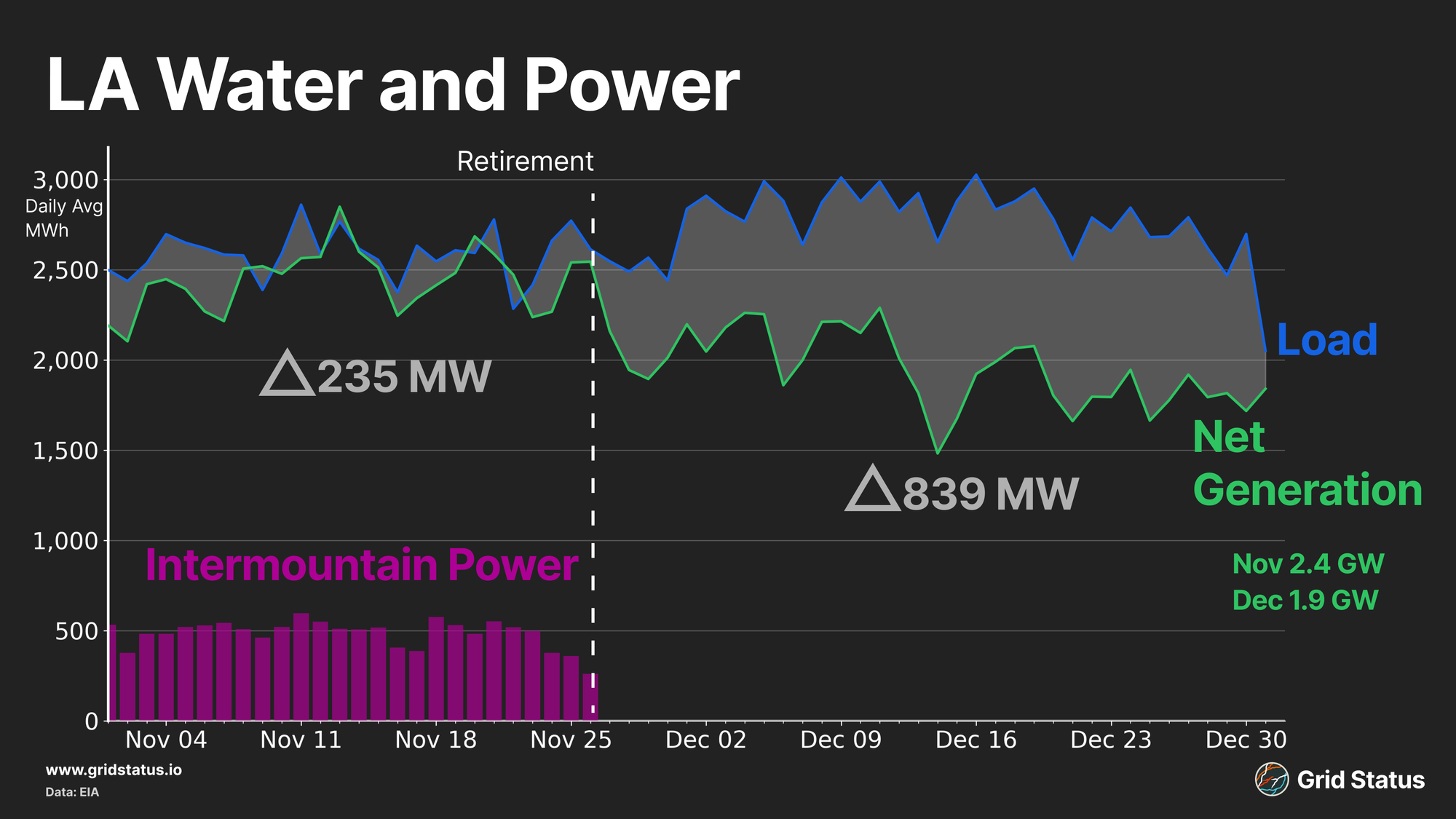

Intermountain Power Plant said goodbye to the grid, and the impacts from this plant coming offline were seen almost immediately. Intermountain served the LA Department of Water and Power (LADWP) to provide baseload generation to the LA area (which is physically within, but administratively without in relation to the broader CAISO grid).

After the plant closure, LADWP’s generation tracked below load and the BA became a net importer. Despite this, the BA remained an exporter to CAISO. While possible impacts are unlikely to materialize during the winter and mild spring, it will be interesting to see how the summer responds in the event of a heat wave. A version of this plant will return, as a conversion to natural gas is planned, so the baseload generation supplied by this plant won’t be lost for too long. Naughton, another coal-fired retirement in neighboring Wyoming is undergoing a similar coal-to-gas conversion.

Merrimack, located in New Hampshire, retired ahead of its planned deactivation date this year, marking the end of coal-fired generation in New England. Even ahead of this plant’s closure, coal had seen a major decline in ISO-NE. A combination of aggressive state renewable portfolio standards, added environmental costs such as RGGI credits, promised offshore wind development, and years of flat load growth made aging coal plants increasingly uncompetitive outside of the most extreme hot or cold days. These pressures have not only impacted coal, with the ISO’s largest gas plant (by nameplate capacity), Mystic, having retired just 2 decades after coming online. Unlike coal’s environmental issues, Mystic’s main issue was economics as it relied on foreign LNG, which tied the plant into the global market vs domestic gas supply.

Unlike other gas plants, Mystic had onsite LNG storage capability, allowing it to avoid having sourcing issues in the winter, giving it the same advantages as coal and oil. The loss of these plants and their onsite storage capacity has complicated operations in New England as offshore wind development has faced multiple development hurdles, and the region’s once stable DC ties with Québec have grown increasingly volatile, particularly during the winter.

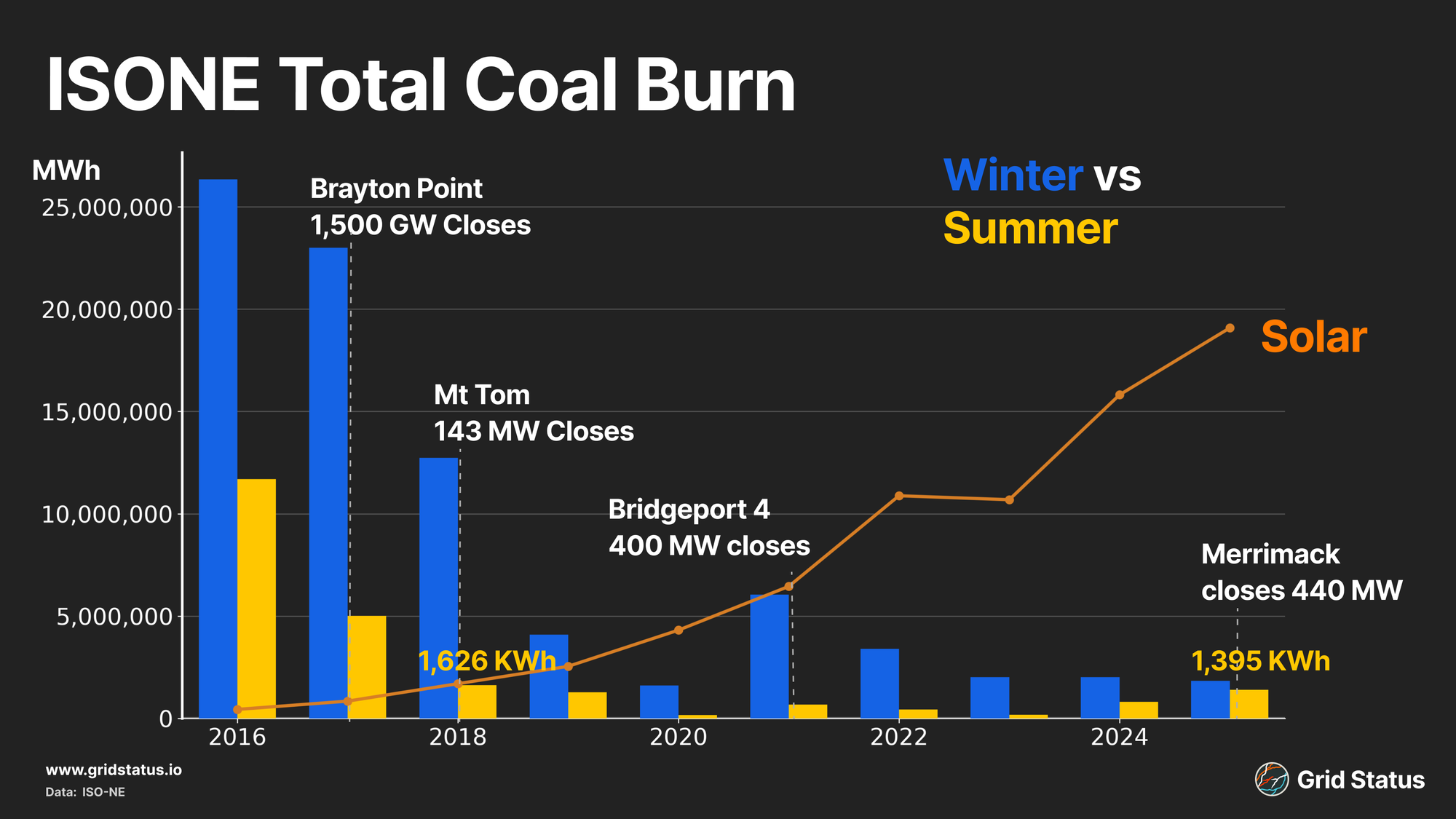

Merrimack marked the last, but certainly not the first, coal retirement for this small grid. Coal saw a significant drop off in generation following the Brayton Point and Mt Tom closures.

Interestingly, coal generation saw an uptick in the winter months following the Bridgeport closure, but gas prices in 2021 had remained elevated following a run in 2020. Summer coal burn in New England this past summer reached its highest levels since 2018 due to an extended heat wave, limiting the ability of the region’s solar expansion to displace as many MWs as has been seen more consistently in some parts of the West.

Looking at the West, Cholla’s retirement came with the fewest obvious grid impacts, although its closure may mark the final years for the remote Arizona town built around the plant. Cholla was originally a 1 GW 4-unit plant that was downsized to 2 units and 400 MW at the time of closure. This plant was located on the border of Arizona and New Mexico, feeding power into APS, serving Phoenix. Despite a large load build-out in the state, generation resources remain plentiful with a variety of thermal and renewable resources to provide supply.

The Desert Southwest saw growth in solar and imports during the midday from California, leading to less of a need for coal, forcing units to derate during the midday hours to make room for solar, while quickly growing battery installations in Arizona have shifted even more solar to darker hours. Older units like Cholla have been facing an increasingly dire economic outlook, leading to retirement. By the time of retirement, Cholla’s units were barely running, with peaking gas units and other, more flexible, coal units supporting the stack. This plant narrowly missed the executive order to prevent future coal plants from retiring, being signed shortly after this plant came offline.

Any plant that retired in 2025 had some grid impact, if only in terms of its exit from the stack, but the circumstances of each varied substantially. Market fundamentals were not the driving force behind what stayed on and what left the grid. Two plants that retired indirectly served CAISO’s market, which has seen an uptick in imports this year, while two others were located on the East Coast near transmission or natural gas limitations. Conversely, small, old F.B. Culley, a 90 MW plant in Indiana, was kept online via a Christmas Eve order.

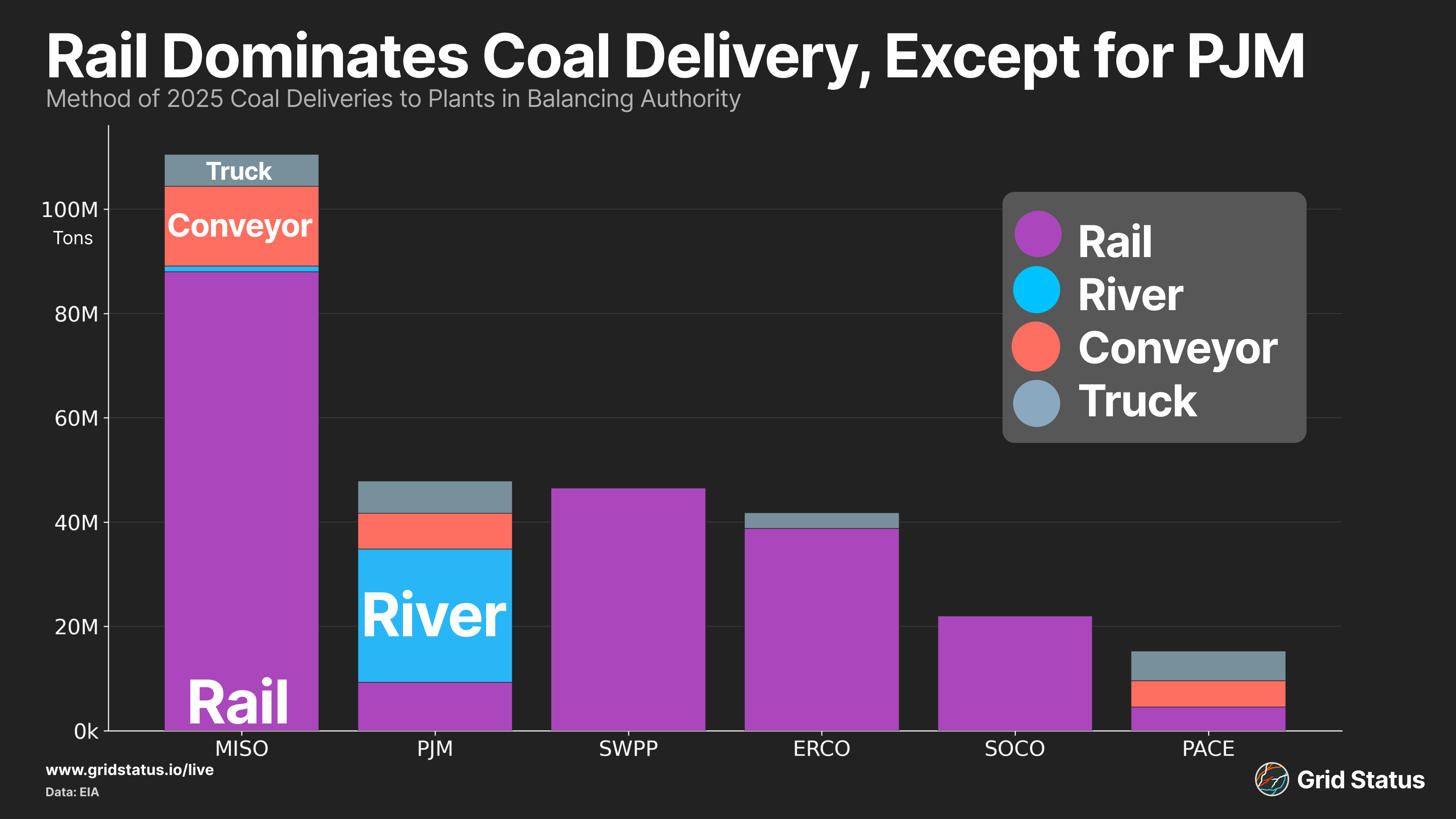

By Rail and By Barge

While gas is displacing coal, it doesn’t travel along the same paths. Coal relies on rail and barge, while natural gas is transported almost exclusively via pipeline with the US. Many natural gas producers even own pipelines, and pipelines only transport natural gas. Conversely, transit via 3rd parties comes with cross-commodity competition and the potential for disruptions such as rail strikes. Five states dominate US coal production: Wyoming, West Virginia, Pennsylvania, Illinois, and Kentucky. Massive surface mines in the Western US account for the majority of coal extraction in the country, and rail is the main transportation method for coal from these locations to power plants.

Rail is the clear leader in transportation, and dominates the large western mines. Barge traffic is a larger player in the eastern US, and particularly in PJM. Major coal plants on the Ohio River receive shipments via Ohio River barges. Winter storm Fern exposed the fragility of barges. Ice built up along the Ohio River as a result of extreme cold temperatures. Beyond rivers, large portions of the Great Lakes, including Lake Erie, have frozen over, which impacts vessel traffic.

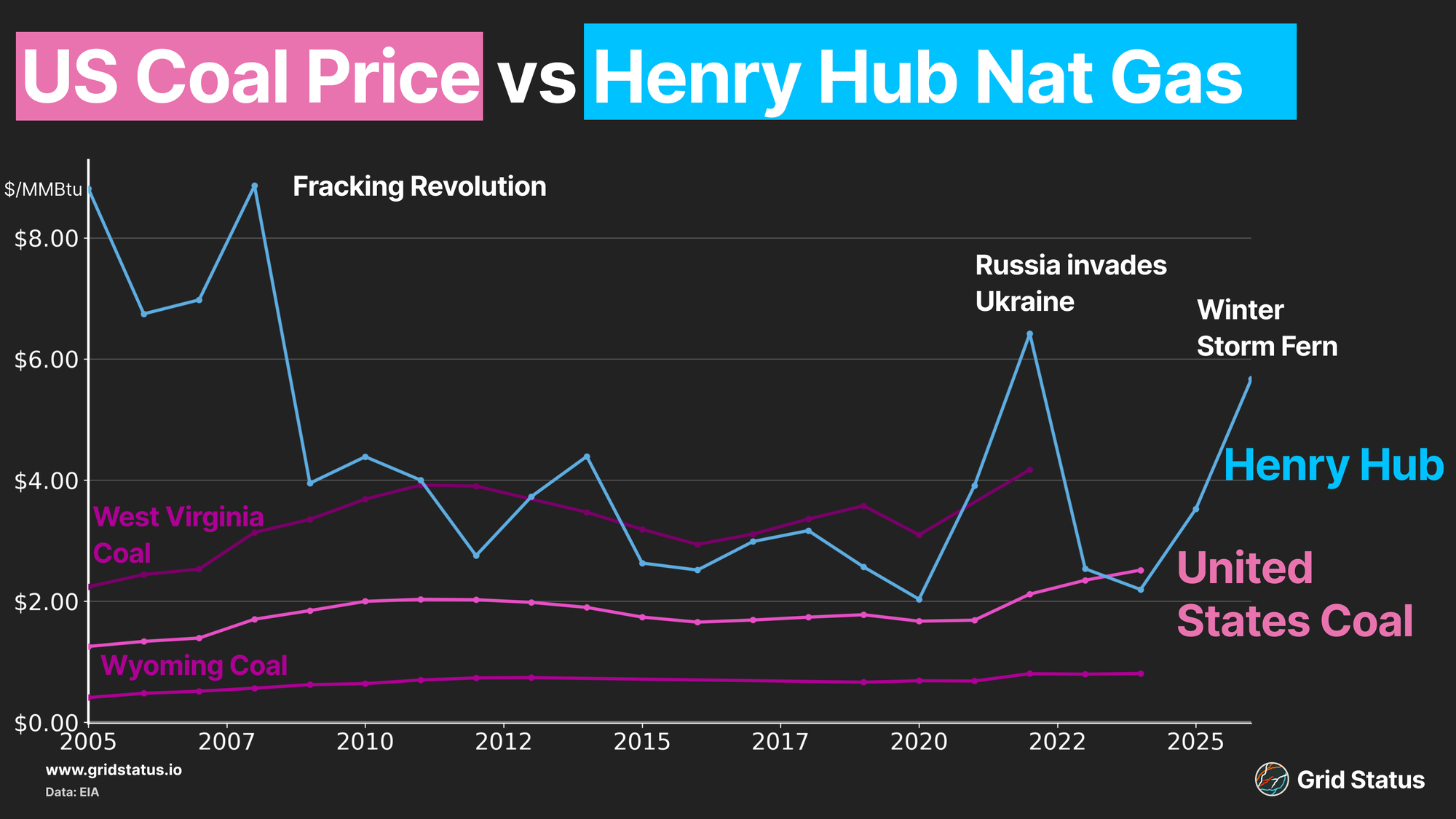

Rail and barge transport is markedly different from pipeline-dominated natural gas transit, often vertically-integrated single-use infrastructure. Coal’s reliance on competitive transit can lead to price impacts during emergent energy crises, with a notable example in 2022. When Russia invaded Ukraine, disrupting the global natural gas market, Henry Hub hit decadal highs.

In the short term, coal became more economical to run, but plants had problems sourcing enough coal to capture the short term upside in power prices.

We have seen the volatility of natural gas spot pricing for years, most recently with winter storm Fern. Coal pricing is generally anchored in longer-term contracts. If a region of the country has a cold winter, leading to an increase in coal burn, coal plants must plan around their already scheduled coal deliveries to ensure fuel supply. Buying coal in the middle of a cold winter can be more difficult due to contract structure.

Mining companies can ramp up operations for increased output within 24 hours, as mines can shift operations for increased profit in the short term (many mines have a reclamation requirement and can stop these efforts temporarily to focus on mining). But the railroads must be willing to open up cars and space for these deliveries, as they can deprioritize coal or even flat out refuse. Coal plants have stockpiles, but must keep a certain minimum level of fuel available per the ISO for reliability requirements.

The differences in logistics between the thermal fuels create an environment where they can act complementary to one another. Providing different levels of support should one resource become constrained physically and subsequently economically. Coal can be stored more readily, while natural gas can be transported more quickly in its just-in-time system with very expensive and limited storage. In fact, this mirrors an older version of the US power system, a vast coal baseload with natural gas balancing. That environment, pre-shale, pre-renewables, is the one in which power markets were conceived of and originally designed. Market development in the context of a more predictable system is having knock-on effects today, with core elements like FTRs struggling to keep up.

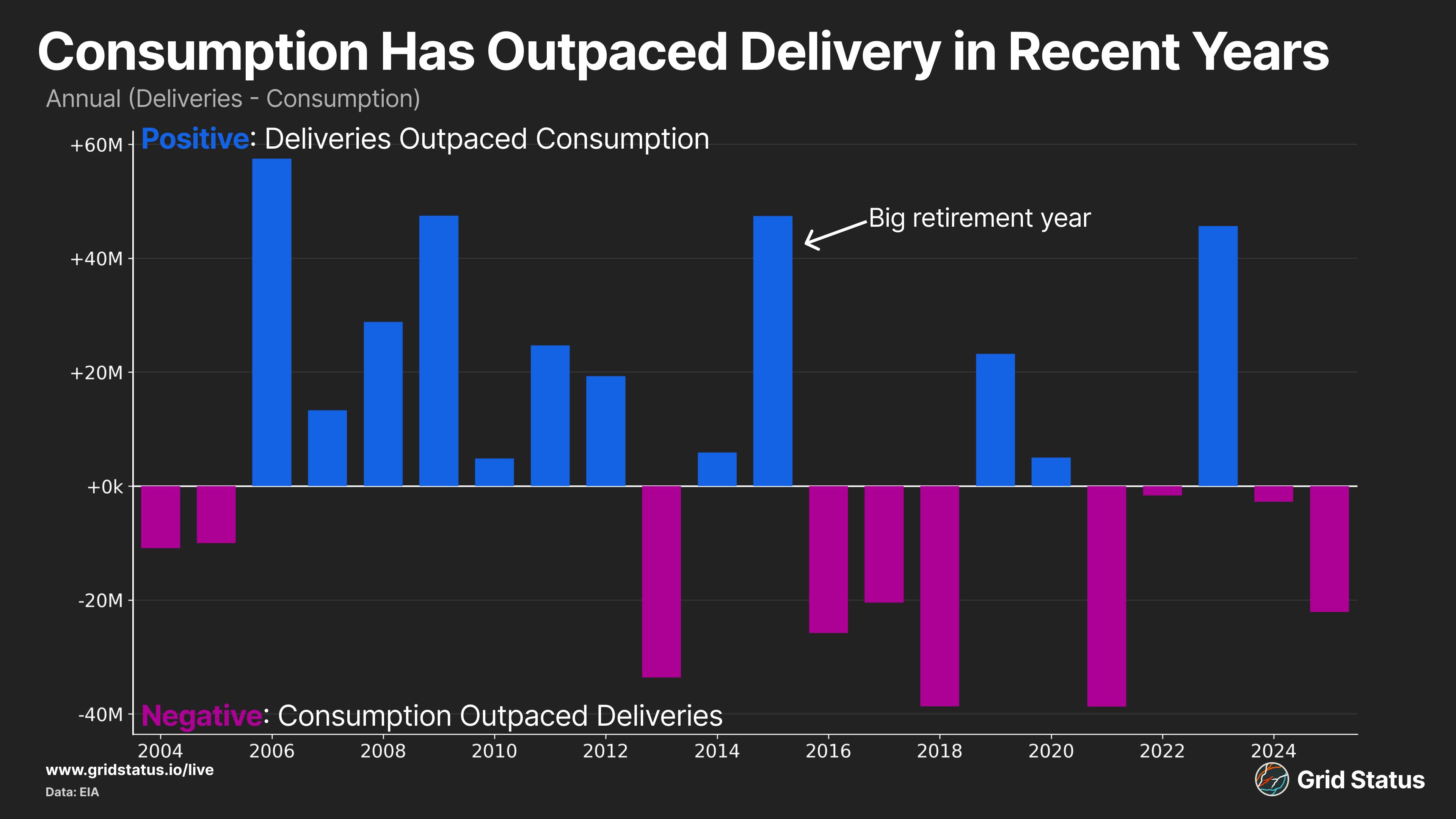

EIA data on coal deliveries to power plants also illuminates another change. As coal generation has declined over the last 20 years, deliveries have, of course, declined, but the relationship between the two has also shifted.

In recent years, consumption has often outpaced deliveries across all plants. This pattern suggests that some plants are running closer to the edge of their stockpiles than they were in the past, and also implies that the owners of coal power plants may believe their current reprieve is short-lived.

Grid by Grid

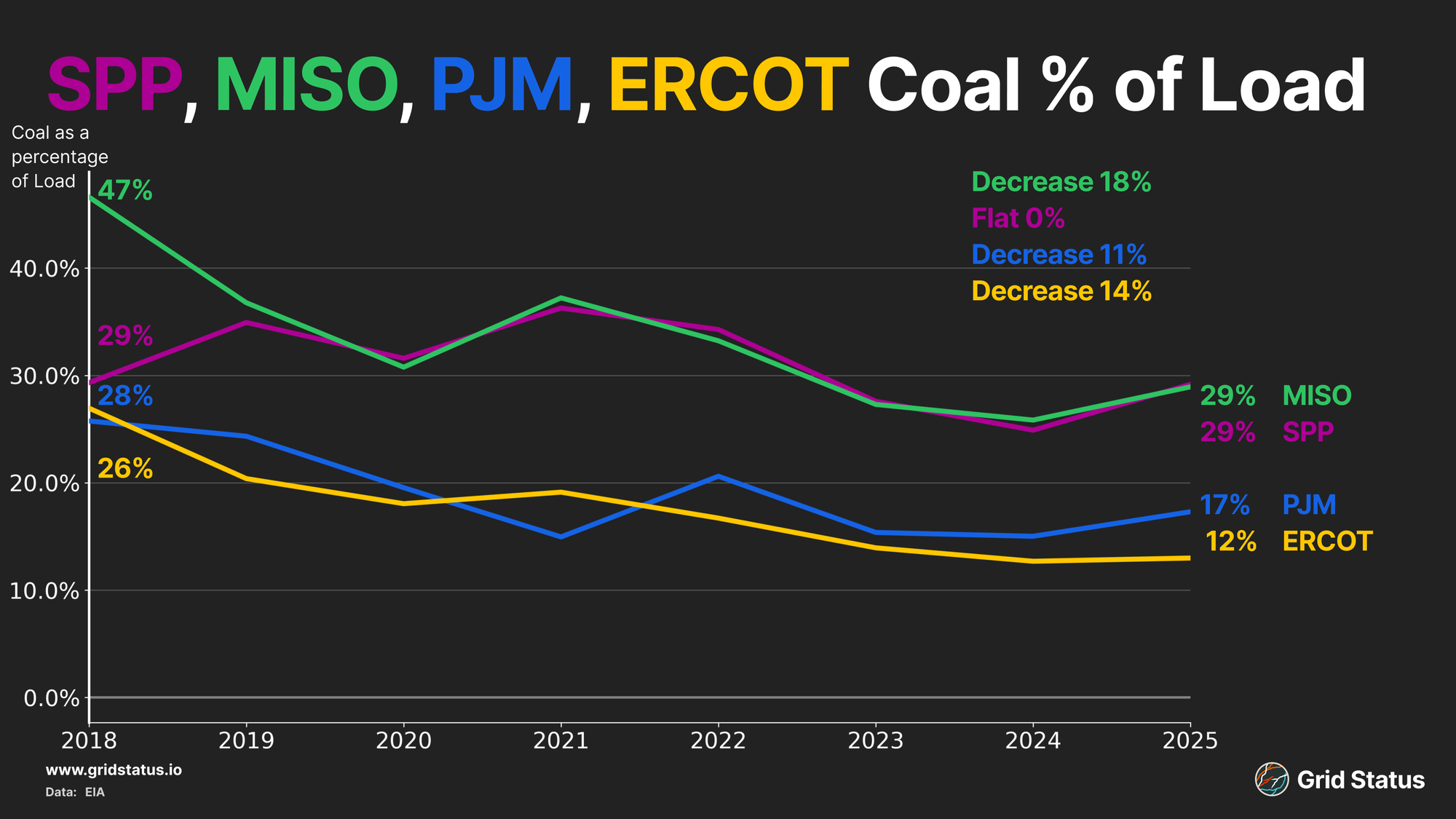

While coal generation has broadly declined, it remains prominent in a few key markets, mainly in the interior of the country. Coal still plays a big role in SPP, MISO, PJM, and ERCOT.

SPP is known for its high winds across the plains, but when the wind dies down, coal generation can take over. In 2025, coal burn actually was up year over year as natural gas prices increased. 2025’s generation even surpassed 2023. Of the Eastern Interconnection markets, SPP has the most direct access to Wyoming mines, and unlike ERCOT, or parts of PJM, relatively less pipeline infrastructure from key fracking basins (although surrounded on all sides by the DJ, Permian, and Marcellus), with the most in-market basin, the Bakken, lying quite far away from traditional load centers in the market.

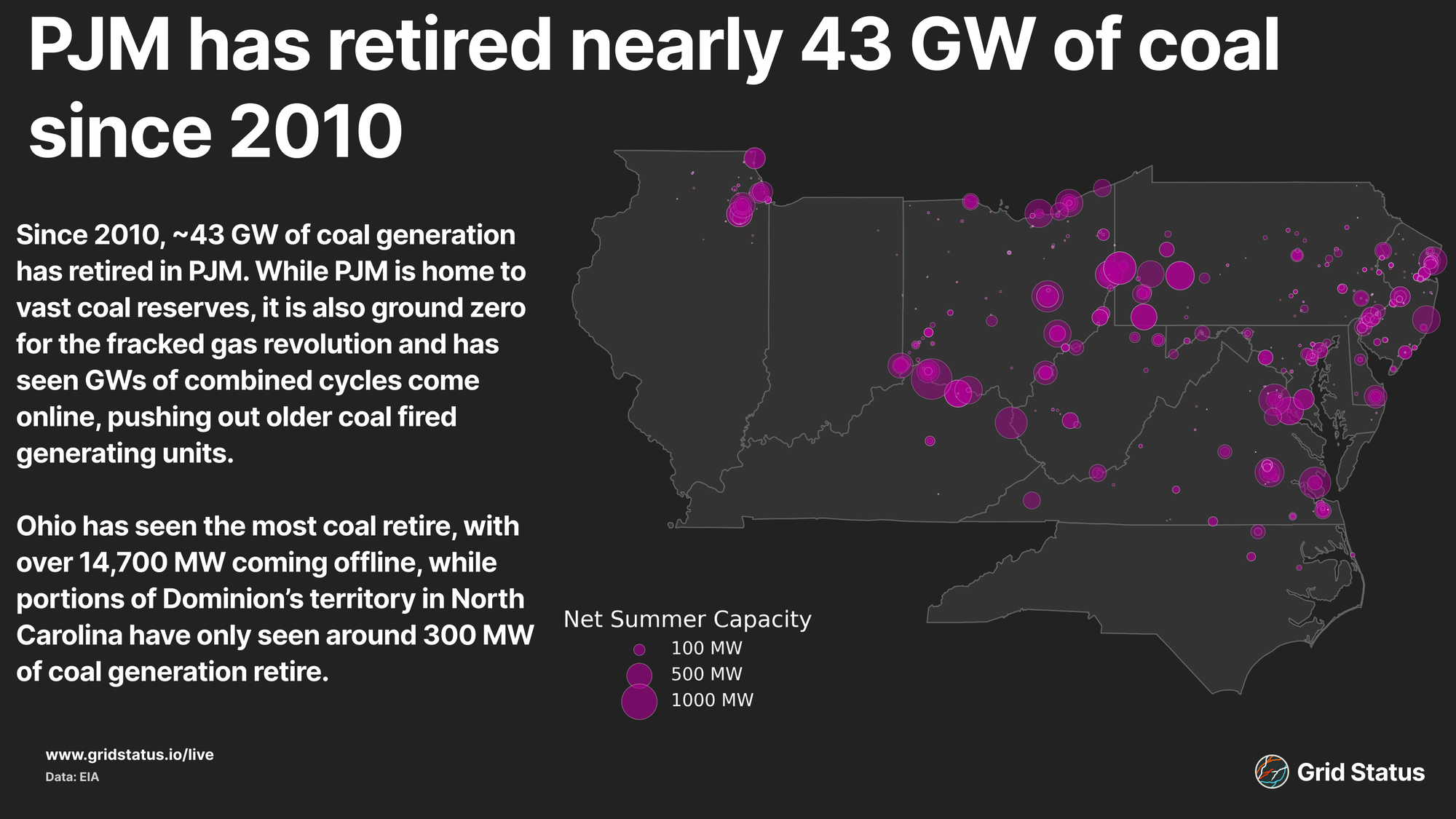

Historically, PJM was dominated by coal-fired generation. In its early power pool days, plants would have had access to shipment by barge and rail from Appalachian mines. Over time, natural gas and nuclear generation took an increasing share of high-capacity-factor generation, and the RTO proper ultimately included nuclear-rich Northern Illinois, lowering coal’s relative capacity on the system. Ultimately, it was PJM’s proximity to Appalachian coal that provided relatively easy access to natural gas, helping spell the downfall of coal in the region.

The growth of hydraulic fracturing made extracting this gas much easier and allowed for a boom in both natural gas production and natural gas–fired generation. Combined-cycle units popped up across PJM, and in states like Pennsylvania and Ohio in particular. The buildout of flexible, new, and importantly, cheap power plants, paired with flat to negative load growth, sent both power and capacity prices downward. Facing both downward economic pressure, aging plants, and increasingly, environmental and regulatory pressure, coal generation quickly began exiting the supply stack. Since 2019, almost 43 GW of coal generation has retired, with additional capacity such as Brandon Shores, being subject to an RMR instead of retiring in 2025.

Much of the drop in capacity is located in the traditional homes of coal generation in PJM: Ohio and Pennsylvania. The two states comprise over half of the region’s lost coal capacity. While much of this can be attributed to access to cheap gas, deindustrialization across the rest belt is also a contributing factor.

In the last decade, MISO has lost about 10.6 GW of its coal fleet, and as the coal fleet decreases, so do the reserve margins. Rush Island, a 1.2 GW coal plant outside of St Louis, delayed their retirement for a while to ensure transmission stability in the local area. This plant did not update its scrubbers to comply with environmental regulations and eventually closed in 2024, 15 years before the original 2039 retirement date. Ameren has recently been approved to build a new simple-cycle gas generation plant and battery. Joppa Coal plant in Illinois also retired early due to litigation related to groundwater contamination from its coal ash pond, retiring 3 years earlier than originally announced.

Capacity pricing in MISO is complicated, with these retirements, sudden large load growth, and substantial changes to the market design, such as changing to a seasonal construct and a graduated, rather than vertical, demand curve. Ultimately, prices have increased to over $600/MW-day in Zone 2, indicating the need for dispatchable generation. While the region has had substantial solar buildout, MISO still has very limited battery storage.

Coal generation as a portion of served load in ERCOT has declined below the other markets, although it may still be surprisingly high given Texas’ lack of internal coal resource, but natural gas is abundant enough to price negative and flare in the far west of the state. ERCOT is also the location of the last large coal plant built in the continental US in 2012.

ERCOT gained attention when the grid failed to deliver reliable power during winter storm Uri. Freezing conditions and a lack of winterization led to widespread natural gas failures across the industry, from the pipelines to the power plants.

Coal might seem immune, but stockpiles can freeze together. Once frozen, conveyance becomes impossible. Coal piles in colder climates utilize chemical sprays to prevent the coal from freezing together, a less expensive short-term solution compared to winterization of the entire natural gas infrastructure stack.

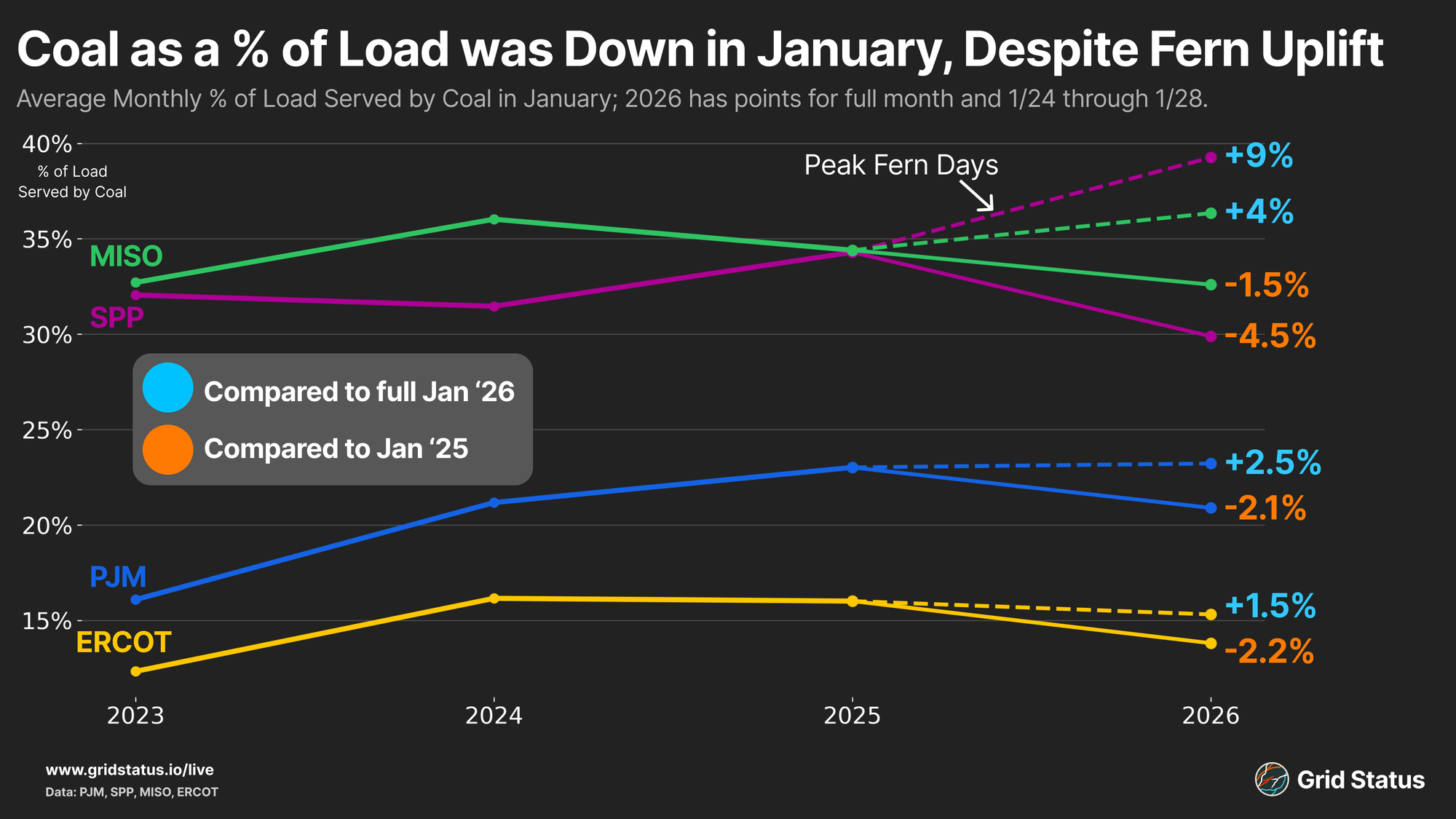

Speaking of winter storms, we can also observe higher coal burn during the recent stretch of Winter Storm Fern. With gas prices soaring due to production freeze-offs and pipeline limitations due to cold weather and residential heating demand, other thermal fuels came online.

MISO and SPP saw an uptick in coal burn compared to earlier in the month, reaching prior-year averages or above. PJM saw coal burn stay consistent as a percent of load despite gas constraints, which is interesting to see as prices suggested a highly strained grid. Despite the Fern pickup, January coal generation ended up below 2025 across all four markets.

Global View

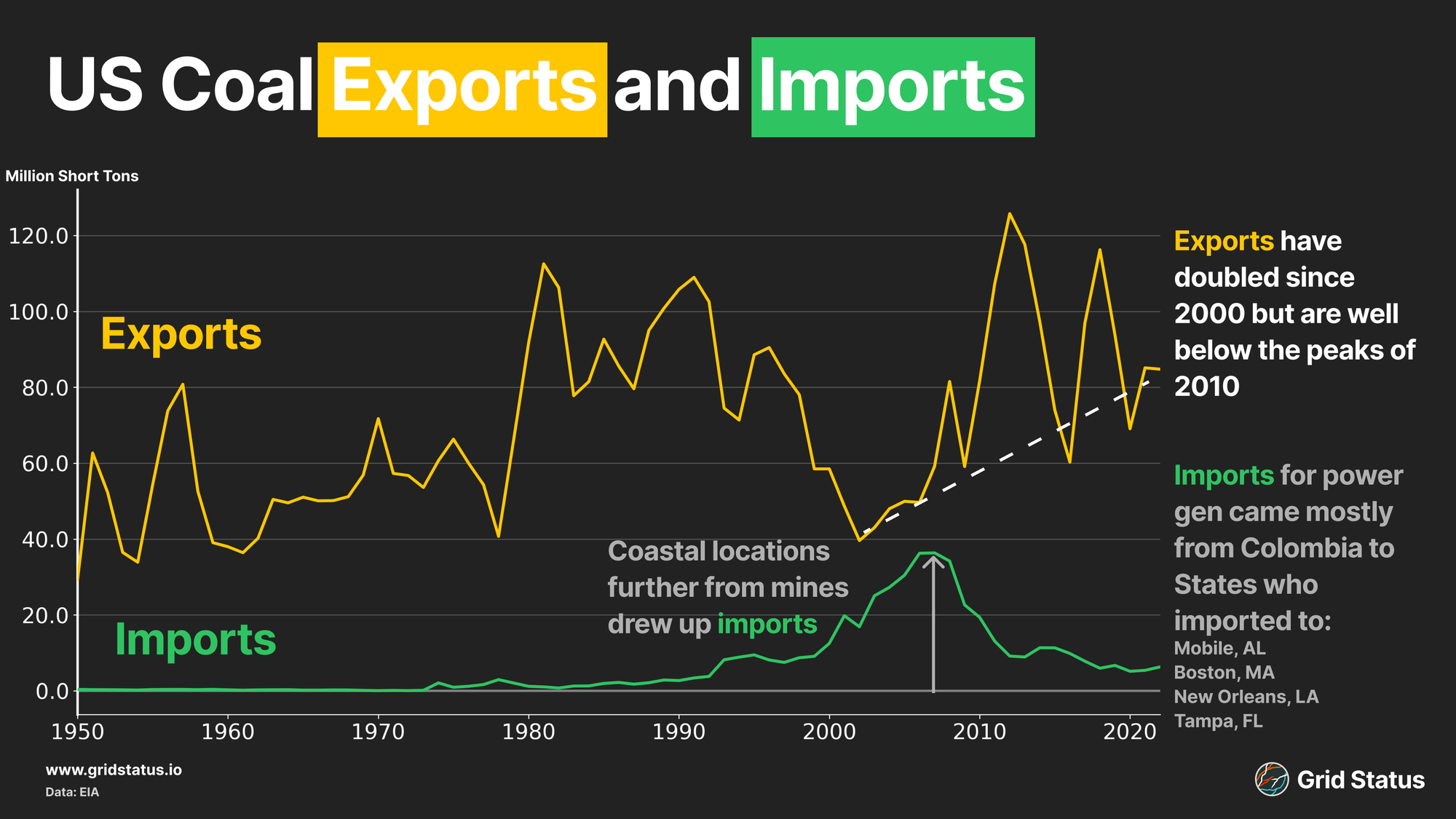

2024 was a record year for coal burn worldwide, reaching 8.77 billionwas tons. 2023 was also a record, as was 2022. If not for the impacts of COVID-19, prior years may have also set records, which is to say, global coal demand has been on an upswing, but this wasn’t always the case. Between 2012 and 2020, demand was relatively flat, but power demand picking up in India, China, and the rest of Asia more than offset declines in Europe and the US. With vast reserves and well-developed mining infrastructure, the US’ international role is as an exporter of coal, making shipments to mostly Asia and Europe.

Annual exports have been volatile, swinging widely based on broader global macroeconomic conditions and energy costs. More surprising to Americans may be the high import values just prior to shale gas. Before coal retirements began in earnest, a number of coastal areas found it easier and cheaper to import coal from abroad, particularly from Colombia. In 2006, Mobile, Alabama peaked at nearly 13M short tons of imports, while Tampa, Florida peaked at 4.7M short tons of imports in 2008.

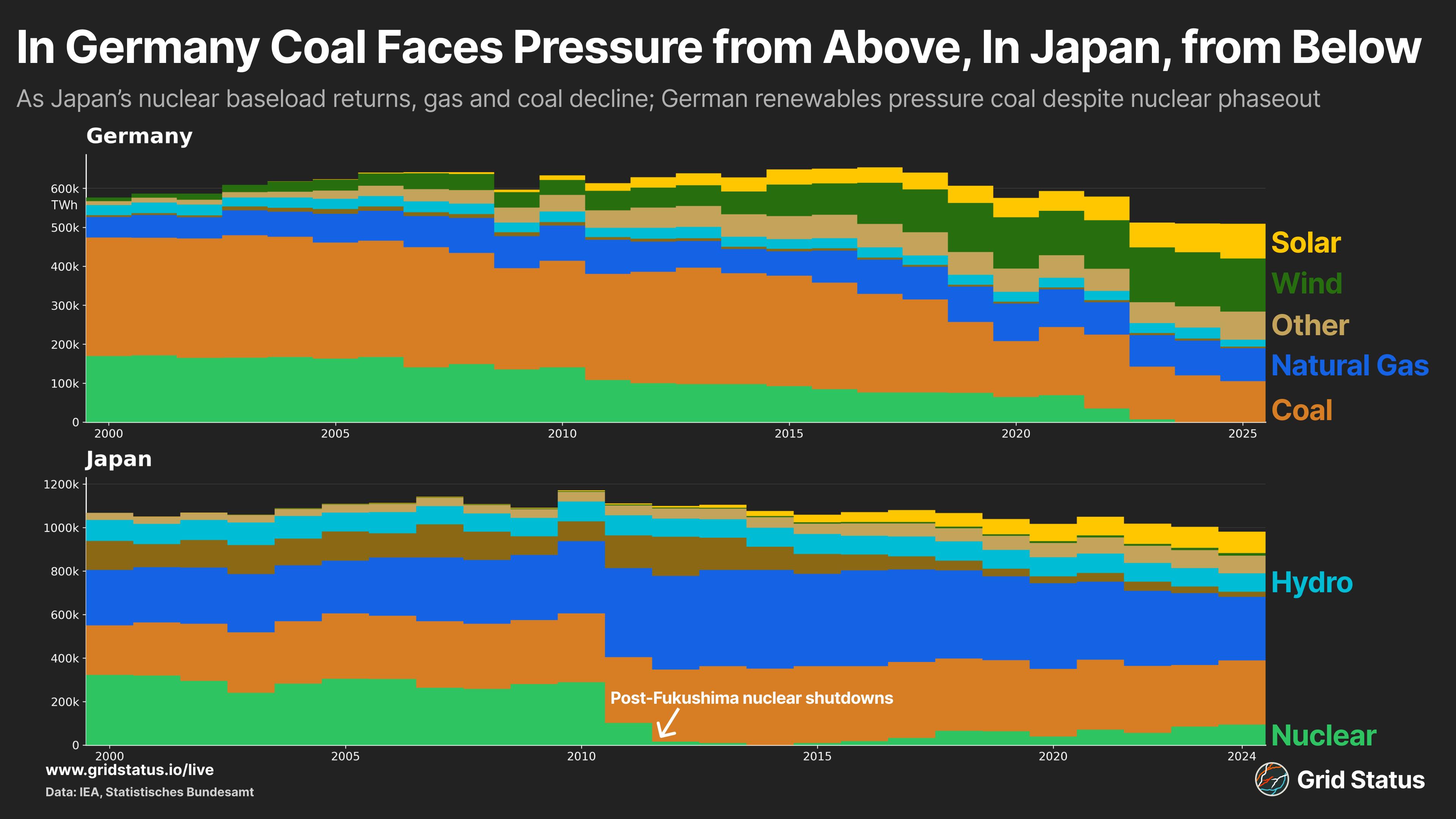

Germany and Japan are the poster children for non-US developed-nation coal strength in energy discourse. For each country, nuclear generation is perhaps the key underlying condition. Japan’s industry shut down following Fukushima, while Germany’s was dismantled as a result of internal politics. In both Germany and Japan, however, coal (and demand!) is on the decline.

In Japan, the return of its nuclear generators directly cuts into coal and gas generation, with more expensive gas plants feeling the pressure first. 2025 and 2026 are likely to see further substantial cuts into gas and coal as larger units have been returning and the buildout of other resources continues.

Conversely, Germany has largely pressured coal from above. German nuclear wasn’t shuttered temporarily, but fully taken out of commission, while solar and wind have been extensively built out. These conditions have led to an international popularization of the Dunkelflaute term (for lengthy periods of simultaneously low wind and solar), and the stubborn fraction of natural gas has positioned Germany to feel acute pressure from price and supply shocks.

Unlike Japan, Germany has numerous coal mines within the country, but not all coal is created equal. In most years, more than two-thirds of coal burned in Germany is high-emitting, moist, lignite. Germany previously produced more lignite than any other country, but has been supplanted by China. The bulk of US production, in comparison, is subbituminous in the West, a step up in energy content, and drier. Higher energy content generally means less “other” in the coal, reducing the potential for certain emissions. Bituminous coal from mines in the eastern US is higher in energy content, but often also higher in sulfur, which can limit its utility.

As less-developed countries move up the industrial ladder, energy options are shifting rapidly. LNG has been marketed as a bridge fuel for developing nations, but building an economy on top of a particularly volatile global commodity can be painful. Just this month, countries across Asia have sought to boost coal generation while throttling LNG-supplied natural gas plants in the face of the US and Israel’s attack on Iran and subsequent closure of the Strait of Hormuz. In Pakistan, we see a split in technologies, with the Power Minister calling for increased domestic coal production, while residential consumers flee the unreliable and expensive grid for small-scale rooftop Chinese solar panels that have flooded the market.

China itself continues to build all of the above, although according to data from Ember, fossil generation may have plateaued over the last year. Even steady, China’s consumption of coal is globally dominant, reaching 58% of all coal, globally (across sectors), in 2024, and one-third of all coal burned for power generation. data the largest contributor in the race to touch the sky, consuming one third of the world’s total coal. So while both China and India saw a year-over-year decline in coal generation in 52 years in 2025, absolute consumption remains extremely high.

Coal’s Plus Ones

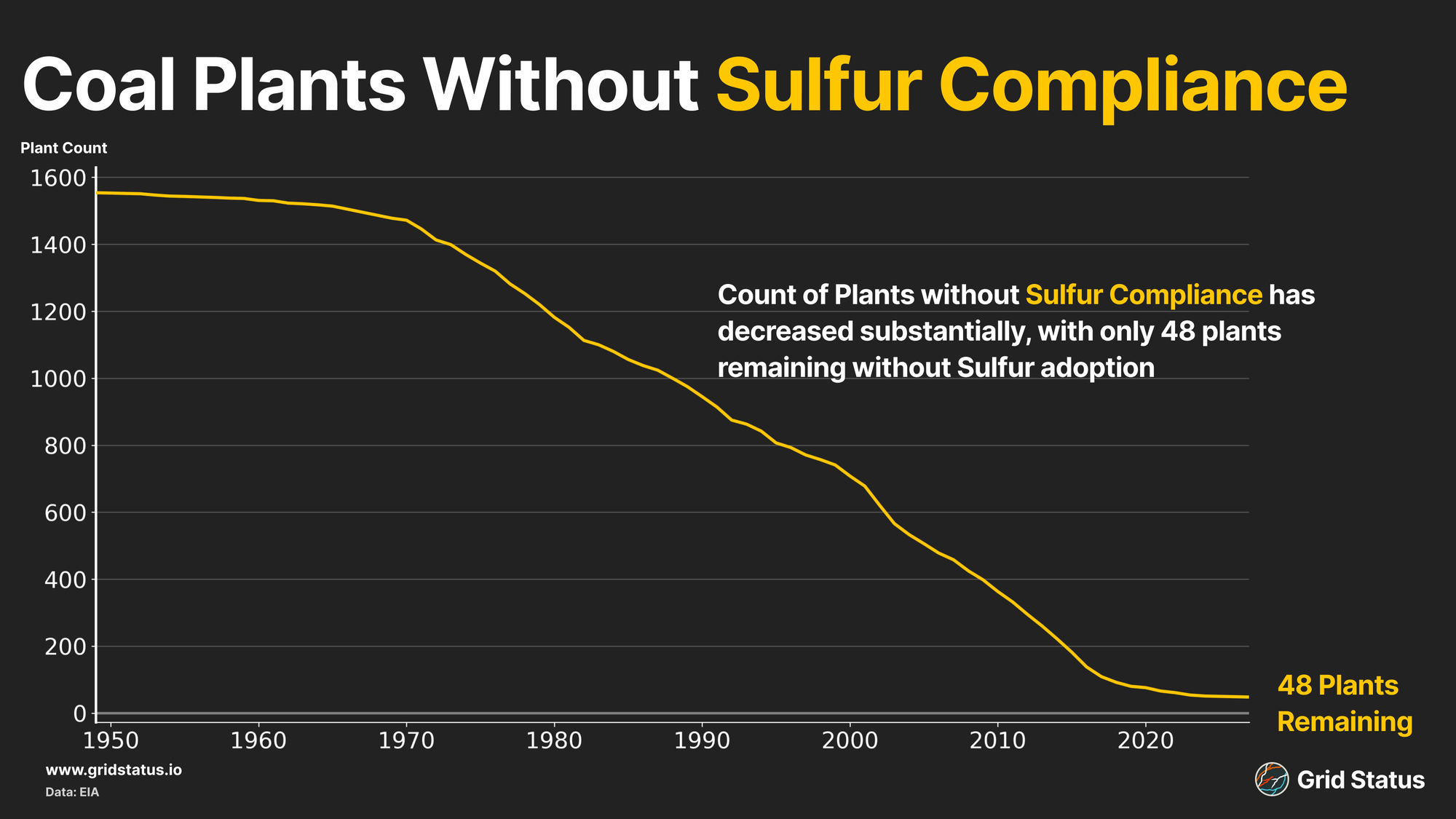

As a solid fuel, coal has baggage. Depending on the classification and rank, different amounts and compositions of water, minerals, and gases come along with the carbon. Everyone knows the story of CO2 (of which coal is the single largest source), and some are aware of the patchwork of carbon markets across the globe, but those other elements in a given lump of coal drive acute health and environmental damage. Since the 1970s, environmental regulation has tackled some facets of these hangers-on, to varying effect. Sulfur, and in turn the formation of Sulfur Oxides, has been one of the more successful stories, albeit not without much wailing and gnashing of teeth amongst the industry. Emission control technologies are why a plant that came online in the 60’s isn’t producing the same emissions it did 60 years ago. Technologies such as Flue Gas Desulfurization Systems, which reduce the SO2 emissions from flue gas generators associated with plant boilers. These systems require power, reducing total output per coal burned, but reducing SO2 is important as it contributes to the formation of ambient particulate matter, which can cause cardiovascular and respiratory disease.

Since 1995, SO2 emissions have dropped by 94%, with nearly all coal plants in the US complying via control technologies.

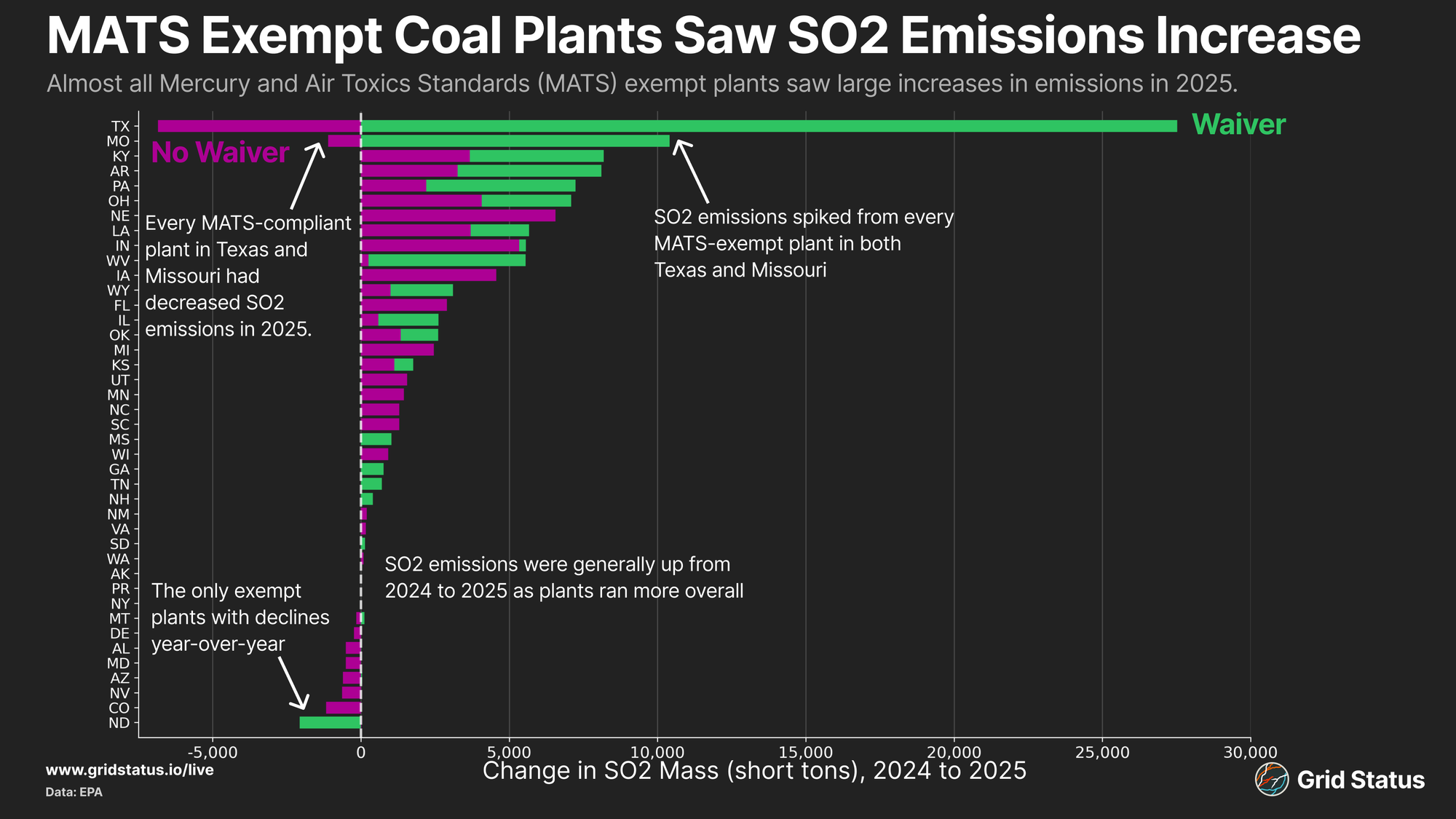

Recently, the WSJ and NRDC (strange bedfellows there) both touched on the increase in coal burn and coal emissions in 2025, citing SO2 emissions increasing substantially year-over-year, both from plants running more in general and seemingly due to emissions waivers and enforcement relaxation. Not SO2 waivers, but exemptions from MATS, Mercury Air Toxics Standards.

Mercury controls have been under discussion for decades, as the combustion process releases it from the coal, and once in the water system, reactions with microbial life convert it to methylmercury, which is able to move through the food chain and bioaccumulate in higher-order species, like humans. Mercury is a neurotoxin that can impair neurological development in the younger population, and with no known safe level of exposure, it can be damaging both to animals and humans. Despite these well-known issues, MATS was not published by the EPA until 2012, during the Obama administration, and then revised to be stricter in 2024, under Biden. The second Trump administration first exempted plants from compliance until 2029 is now rolling back the 2024 update entirely, which would have reduced Mercury emissions by 70% from 2012 levels.

In 2025, the presidential exemption is clearly visible in emissions data.

Plants in Texas and Missouri top the list for increased SO2 output, while the only facilities with declines in those states do appear on the list of exemptions. Coal plants overall ran more, but the rate of SO2 output also changed for a number of facilities.

Power plant GHG standards under Clean Air Act section 111 are also being rolled back, with the endangerment finding currently on the chopping block. The strategy here is no longer rooted in science, but in finding phrases that provide legal cover to dismantle regulations regardless of impact. Many coal plants had been planning to retire rather than install control technologies to deal with CO2, so an extension of the recent transportation emissions rollback to power would likely extend the life of many coal power plants.

What about new technologies that could help make coal even ‘cleaner’ for the environment? In 2013, we saw the Duke Edwardsport Integrated Gasification Combined Cycle coal-fired power plant attempt this. Blowing out to double their budget, the result was a facility that cost more than $3 Billion failed to achieve its initial design goals. CCS has been shown in practice, but not yet applied at scale to power plant emissions. So while nearly all plants in the US today are lower-emitting than their mid-century forebears, a long and difficult path remains to actually eliminate damage to human health. Today, this journey is clearly not a priority for regulators in the US.

An Unpredictable Path Ahead

In the short term, coal has tailwinds in the US and abroad. In fact, it’s possible that the attacks on Iran were the single most impactful pro-coal policy decision the Trump administration has made to date. Reminding the world of the difficulties associated with storing and transporting liquids and gas through highly concentrated corridors of supply with a history of instability can be a powerful motivator to cling to coal

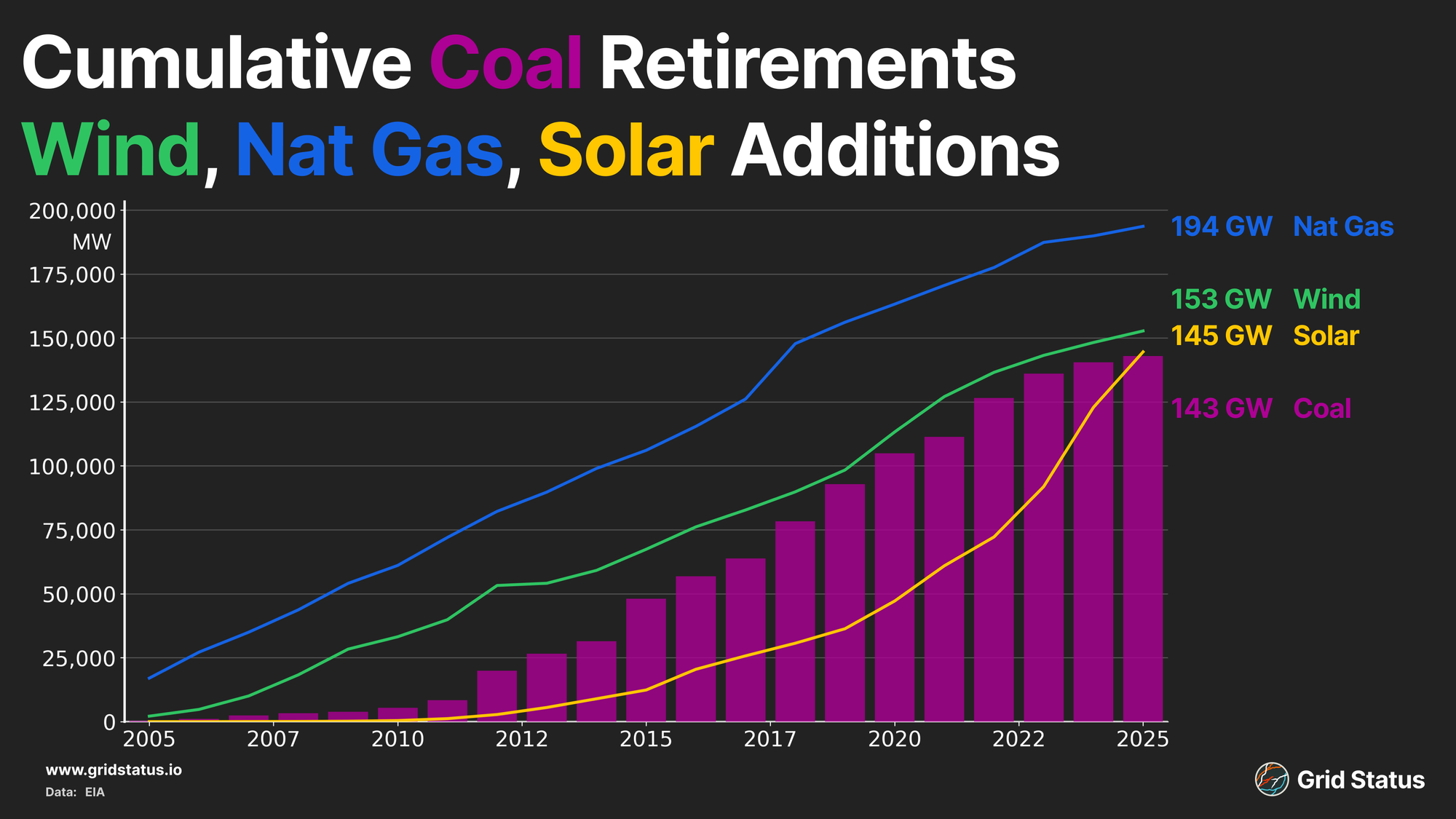

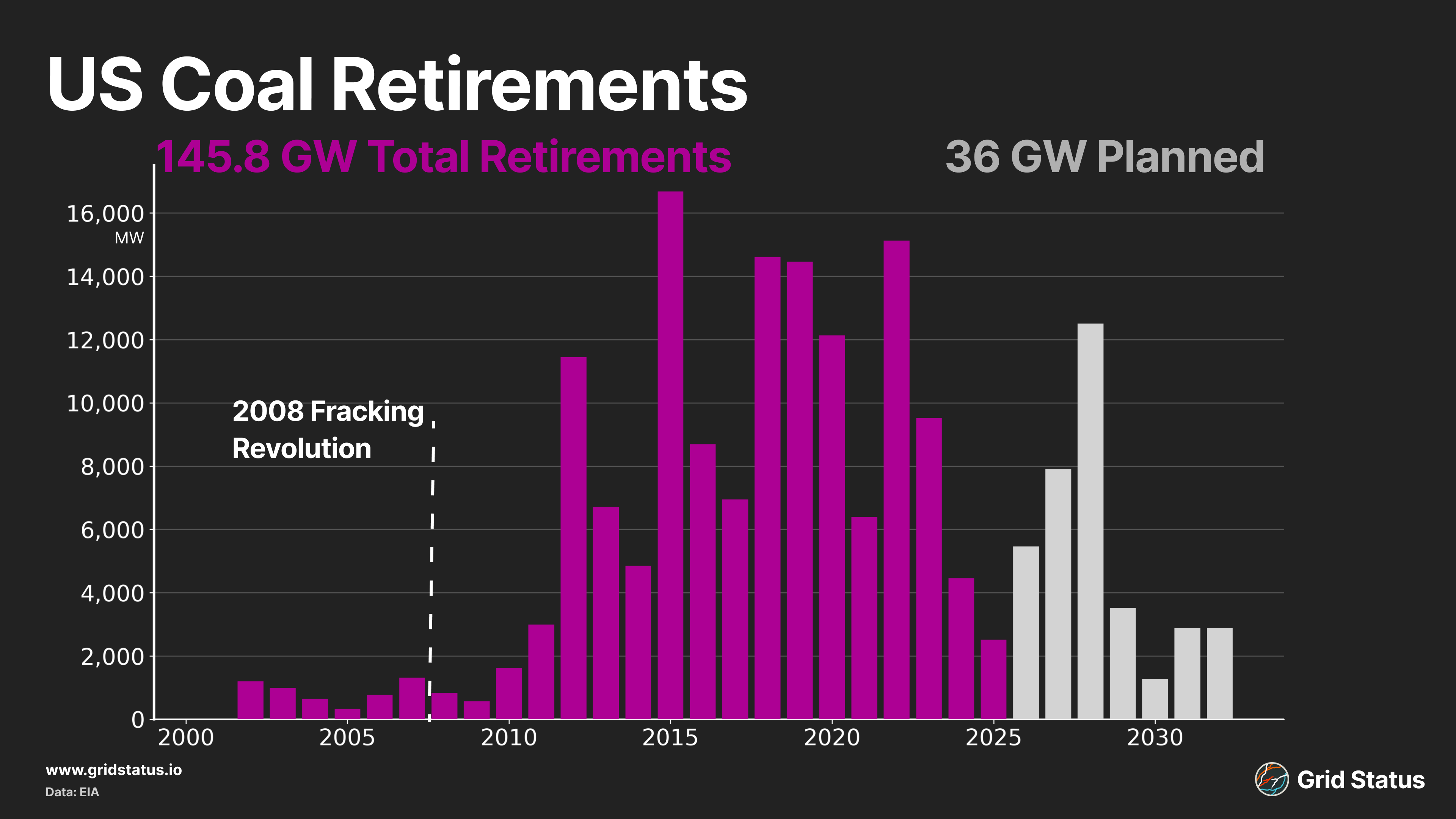

On the flip side, the US has retired nearly 150 GW of coal capacity, and the last plant to be built was six years ago, in Railbelt Alaska, near (for Alaska) a mine, and replacing an older plant in the same spot. Meanwhile, that same reach for stability could trigger demand destruction for fossil fuels entirely. After all, everywhere has access to sun and wind, allowing some freedom from the whims of ancient life and geology.

The EIA's latest numbers show 36 GW of retirements planned between now and 2032, but that’s following the lowest capacity-retirement year in a decade. The 2032 coal closeout looks like it might not verify, as existing plants are supported by high capacity prices, queue difficulties, and a data center industry creating a turbine backlog for behind-the-meter power alone.

For the immediate future, all signs point to continued extensions of existing plants. While the twin forces of Trump 2.0 and load growth seem unlikely to abate in the immediate future, it’s important to keep in mind that retiring any part of the energy system is fundamentally difficult. Many observers have noted that historically we’ve layered new systems on top of old, rarely reaching complete excision. Where it has come, regions have taken different paths. Just in North America we have CAISO’s monomaniacal focus on new technologies while maintaining strong regional interconnections, Ontario’s pivot to focus on the baseload they already had in excess, or a market like NYISO where coal had become uneconomic relative to gas and the state had big future plans.

Which path, if any, other regions take will depend on the particular milieu of policy, price, and options. We’ll be tracking the markets and resources as they continue to evolve over the coming years, so stay tuned and stay informed.