Off to the races: Starting line of EDAM

The West saw another market change earlier this month with the launch of EDAM. We break down the first few days of Day-Ahead clears, anomalies, new market products, and what the future holds.

CAISO’s much-anticipated Extended Day Ahead Market went live just two weeks ago with its first participants. We’ve been tracking these developments for years and published a deep dive last October. Now that the market is off and running, we’re taking a look at how things are shaking out.

We'll get into price clears, the GHG components, regional flows, the ongoing issues with congestion allocation, and more. Alongside a new market comes new (and familiar) terminology, so check out the drop-downs throughout for a refresher on what you need to know.

You can also watch live EDAM outcomes on our new EDAM tab, off of the CAISO Live Page.

Brief Overview

Pacificorp East and West (PACW & PACE) were the first balancing authorities in the West to join EDAM. So far, the market launch has seemed relatively smooth, and Pacificorp won’t be alone for long, with Portland General Electric (PGE) expected to join later this year. EDAM is not a full RTO as members retain control of resource planning, reliability, and transmission line operations. This change does introduce a Day Ahead price element in the west, where the majority of BAAs previously only had exposure to a real-time balancing market.

The Day Ahead price doesn’t just include energy, but encompasses a couple of different elements. The DA Locational Marginal Price (LMP) = energy cost + congestion cost + losses + greenhouse gas (GHG). DA bids are financial only; DA awards impact real-time position with awards for energy, translating to the resource schedule. Reliability Capacity is a new portion of the market to ensure adequate physical supply, which allows BA's for both upward and downward dispatch.

Elements in the Day Ahead Market:

RSE (Resource Sufficiency Evaluation) - occurs at 10 am before the Day-Ahead market is run. Evaluates the offered supply from Pacificorp to demand, imbalance reserve, and ancillary services for each hour in the DA.

GHG (Greenhouse Gas) - a regulatory model that incorporates a price adder to participating markets in an effort to reduce emissions

MPM (Market Power Mitigation) - if there is is localized congestion, then MPM lowers bids in regions to help keep prices to be competitive throughout the system. The system will look at the bids based on Energy and Imbalance reserve to move it into the IFM process

IFM (Integrated Forward Market)- clears bid-in supply against the bid-in demand(due to price imbalances caused by congestion), first phase of EDAM the ancillary services will be self-provided. Requirements will be procured on an hourly basis based on load forecast, solar and wind forecasts.

RUC (Residual Unit Commitment) - provides dispatch capability to make sure that the physical supply scheduled in the day-ahead meets demand. ensures reliability, capacity awards and schedules reliability capacity transfers

The Starting Line: The First Day

While go-live was May 1st, activities began on April 30th with the first day-ahead submission. Submissions close at 10 AM, and the price clear is supposed to be posted around 1 PM Pacific time, but was delayed a couple of hours (CAISO stated the delay was for data verification purposes). Delays for initial data publication tend to be a fact of life for big market changes.

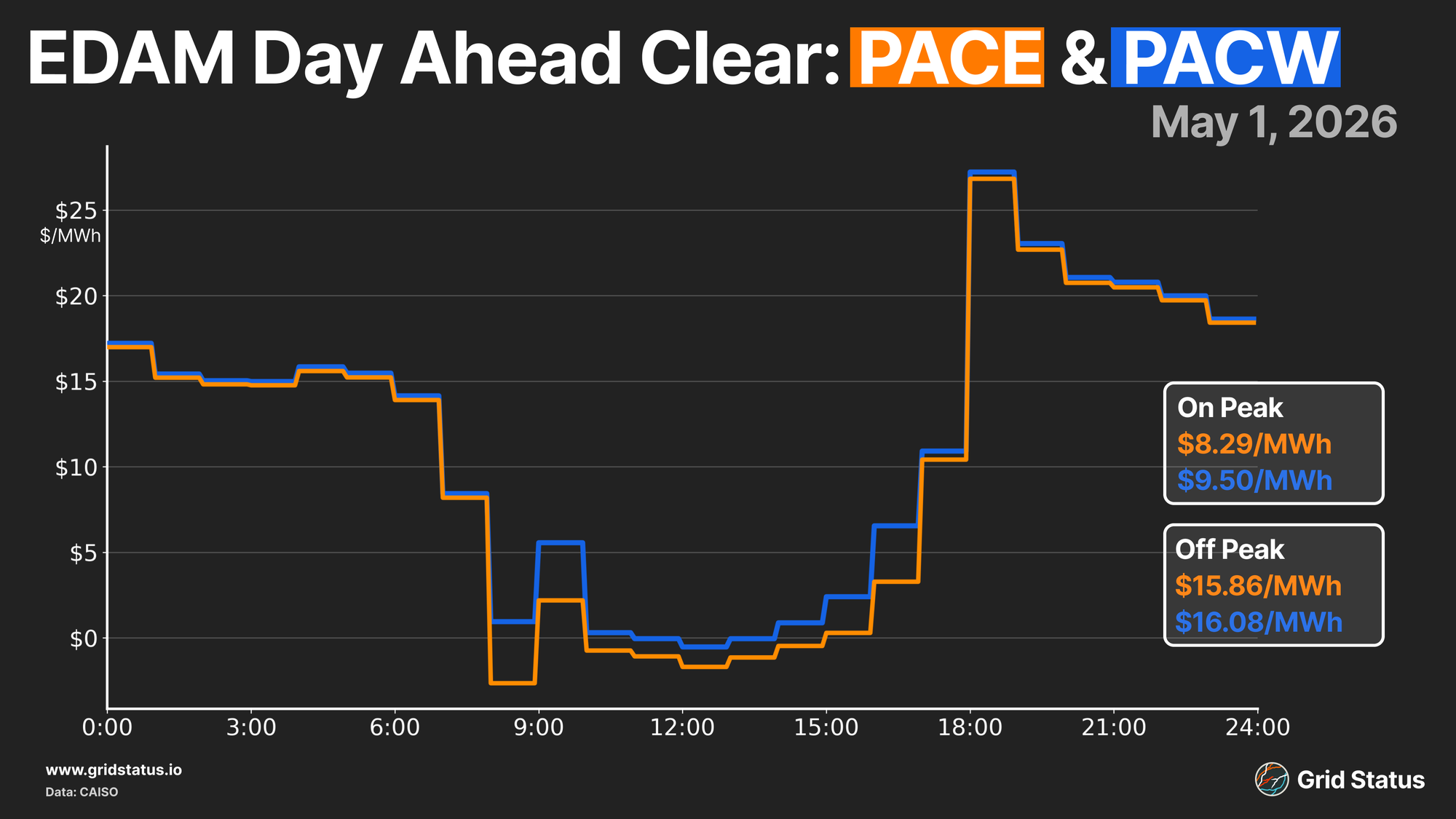

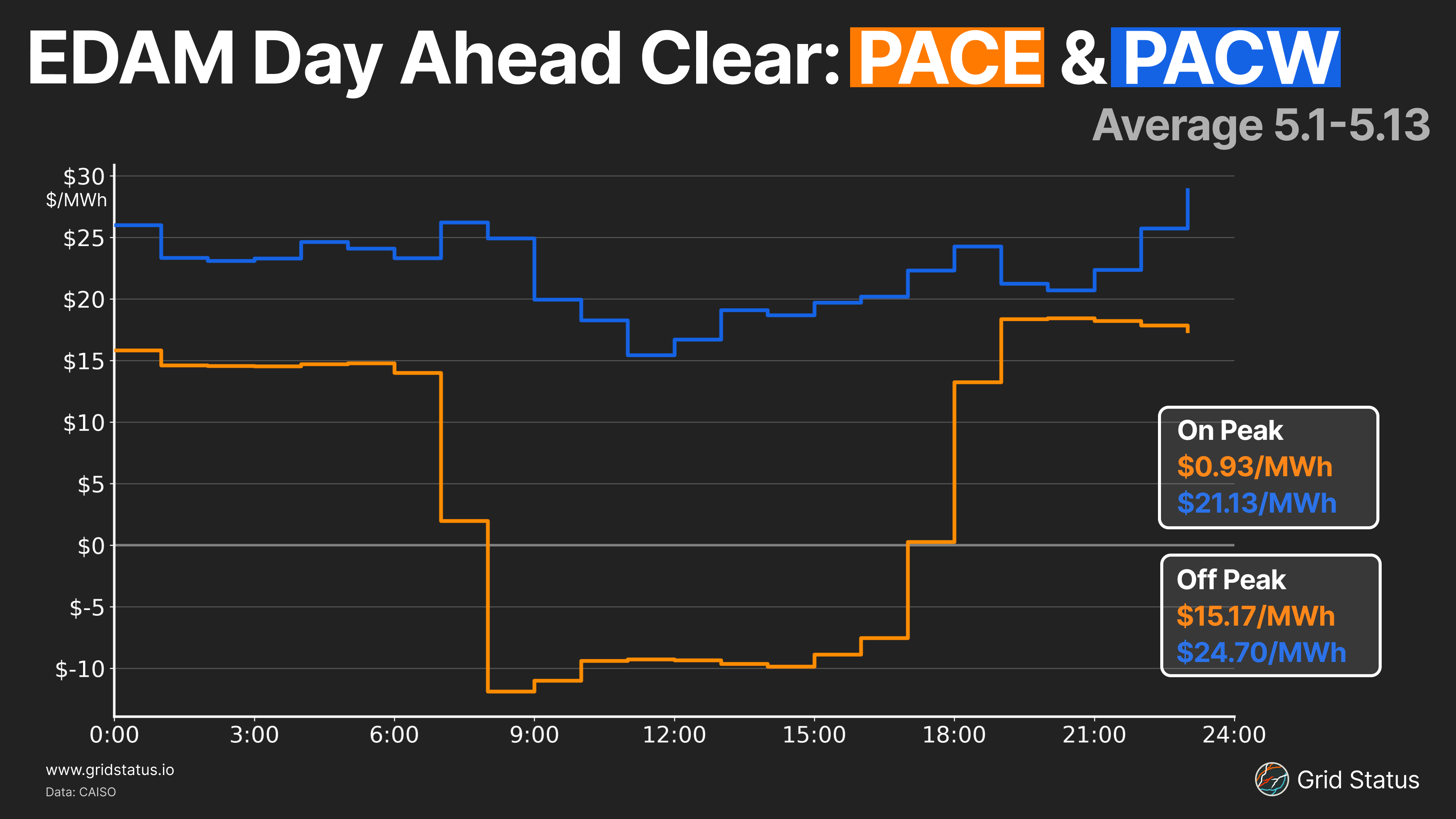

The aggregated prices for PACW and PACE cleared near their real-time April average in WEIM (Western Energy Imbalance Market) and saw a midday price trough driven by solar generation. PACW did see some elevated DA pricing through the midday, but the peaks and off-peak periods for PACW and PACE were in line for this first day. Overall, prices for both balancing authorities tracked closely to one another throughout the first day despite some larger differences in the fuel mixes.

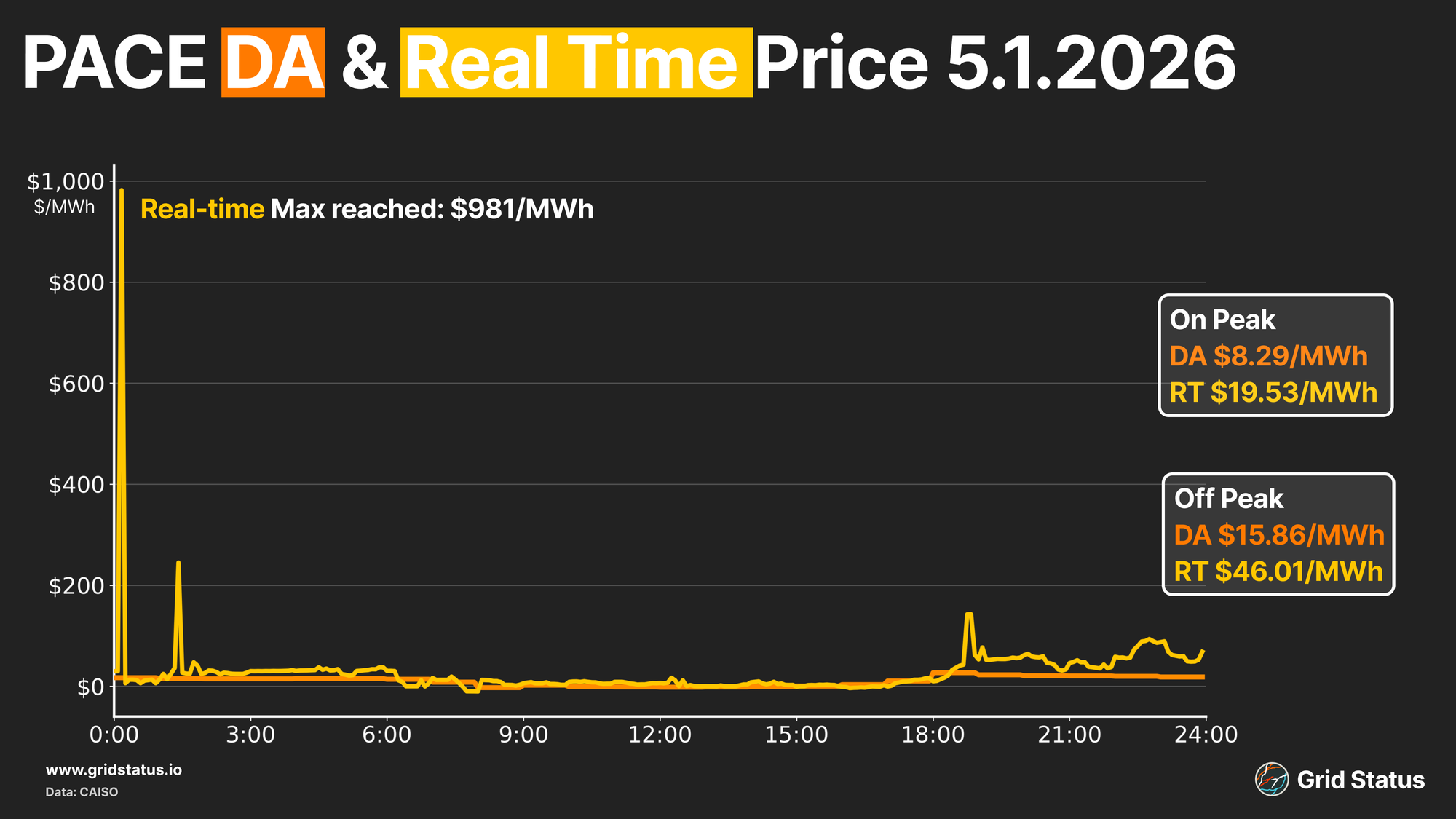

Unlike the day-ahead synchronicity, real-time prices displayed volatility on the first day, with a -$16.78MW/h PACE DART, driven by a price spike as the market turned over at midnight, as well as price strength during the evening peak. The midday saw some moderate price strength.

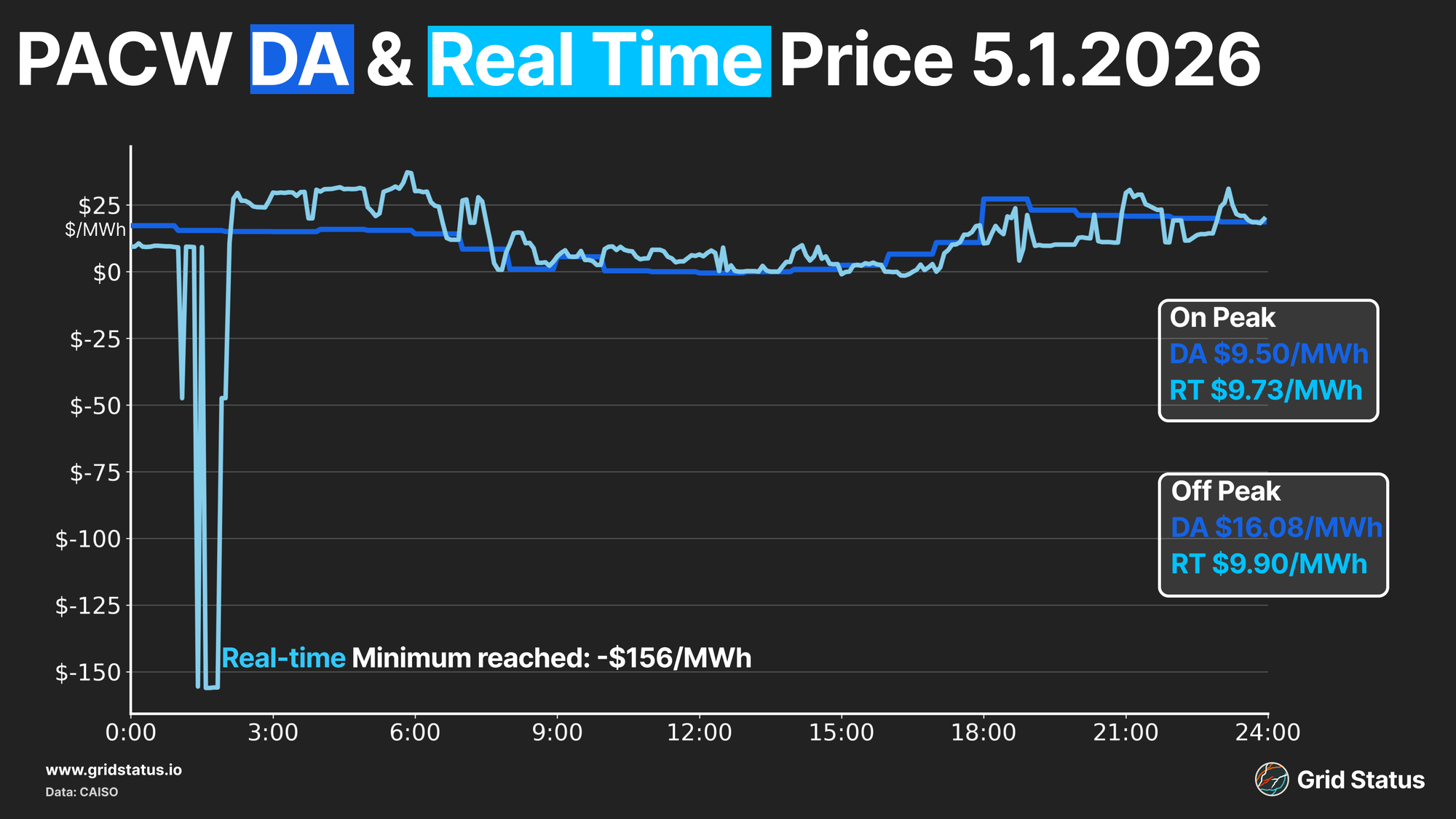

The first few hours of real-time operations in PACW were defined by bearish pricing. RT prices dropped as low as -$156/MWh, before largely tracking above the DA clear until the evening.

Real-time prices showed moderate strength in the remainder of the off-peak, but overall tracked closer to the Day Ahead clear, seen in a much shallower $1.64/MWh DART spread.

Competitors’ Strategy: Two Different Grids

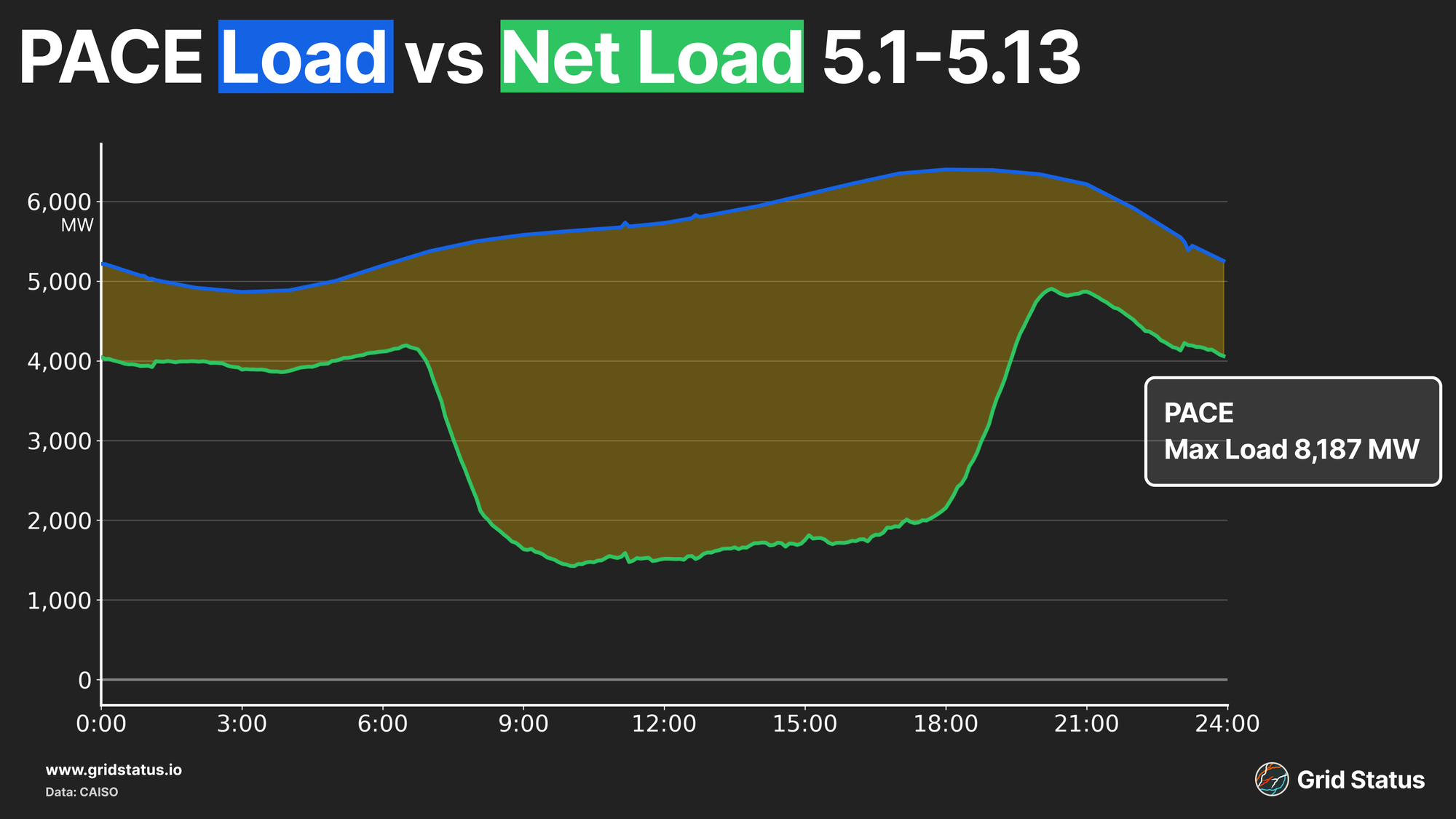

Pacificorp is divided into a West and an East side. Towards the east, PACE has a larger load footprint, more than twice the typical demand of PACW. PACE’s territory is located primarily in Utah and Wyoming, resulting in greater access to solar and wind which leads to a substantial midday trough. Higher levels of utility-scale solar, lead to deep net load troughs. This leads to heightened thermal ramping leading into the evening peak and potential for price volatility.

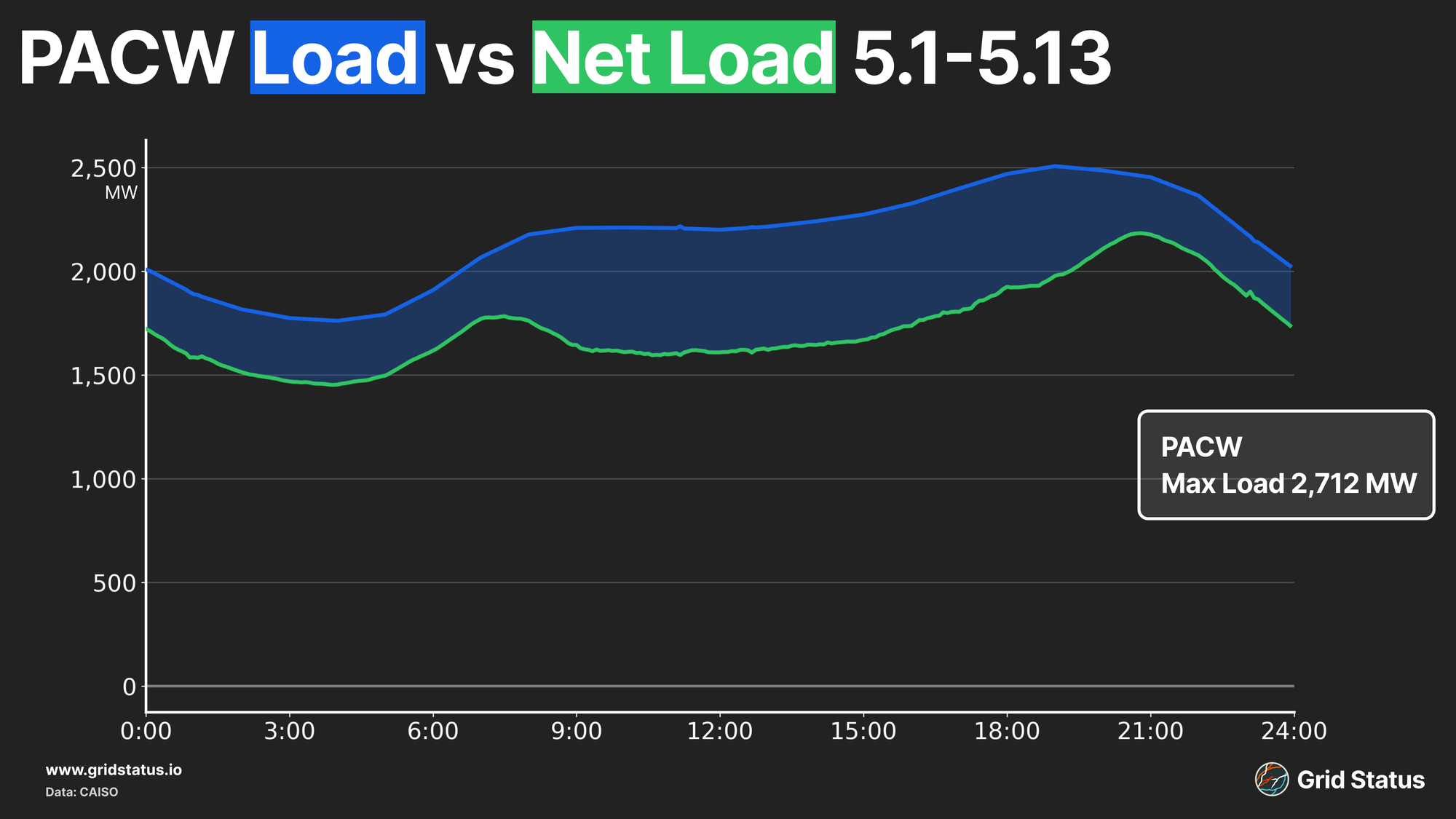

PACW, the western of the two, is primarily located in Oregon but has some assets spread between both Washington and portions of Northern Idaho. Compared to the other half of the BA, PACW has lower load, and wind and solar penetration. This means that net load levels track the overall load much more closely. Despite low levels of inverter-based resources, PACW is home to large levels of renewables, mainly hydro along the Columbia River.

With differences in the respective resource bases, the DA clears have not maintained their day-one similarities but have diverged greatly.

On average, Day-Ahead prices in PACE have been negative during the daytime hours due to an influx of solar generation.

This leads to an almost $20 spread between the on and off-peak. On the other hand, PACW prices have been much more stable, due to more dispatchable generation in the form of hydro. Daytime prices only show about a $3 difference between the on and off-peak periods.

What’s new in the neighborhood

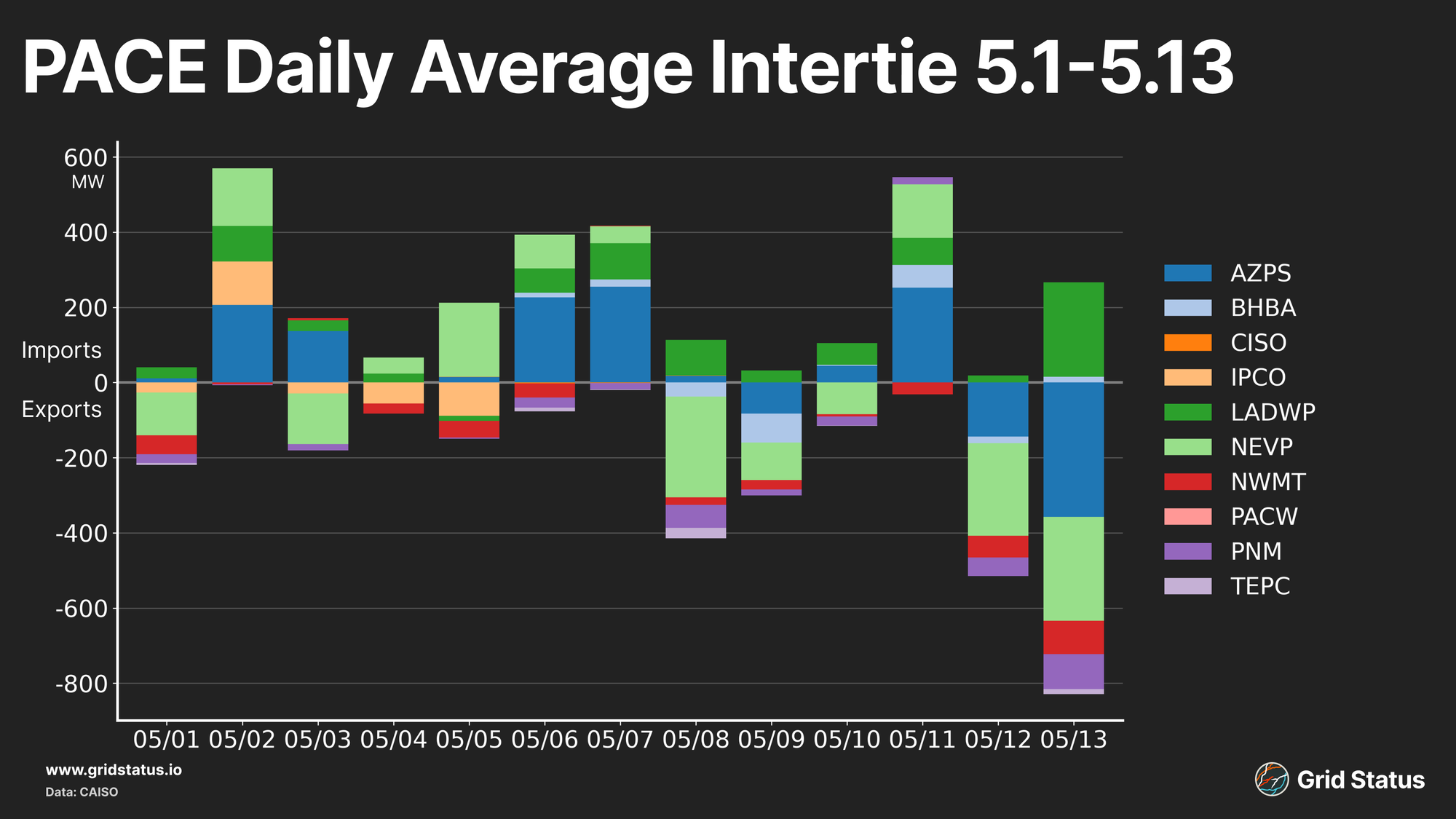

Pacificorp doesn’t operate on an island, and has plenty of neighbors that see implications from their move towards more fulsome market integration. Notably, PACE and PACE share no direct connections, and any power flows must flow through Idaho Power. To add to the complications, Idaho Power is not currently participating in a DA market, but is likely watching this EDAM launch closely on whether to commit to CAISO’s EDAM or SPP’s Market+.

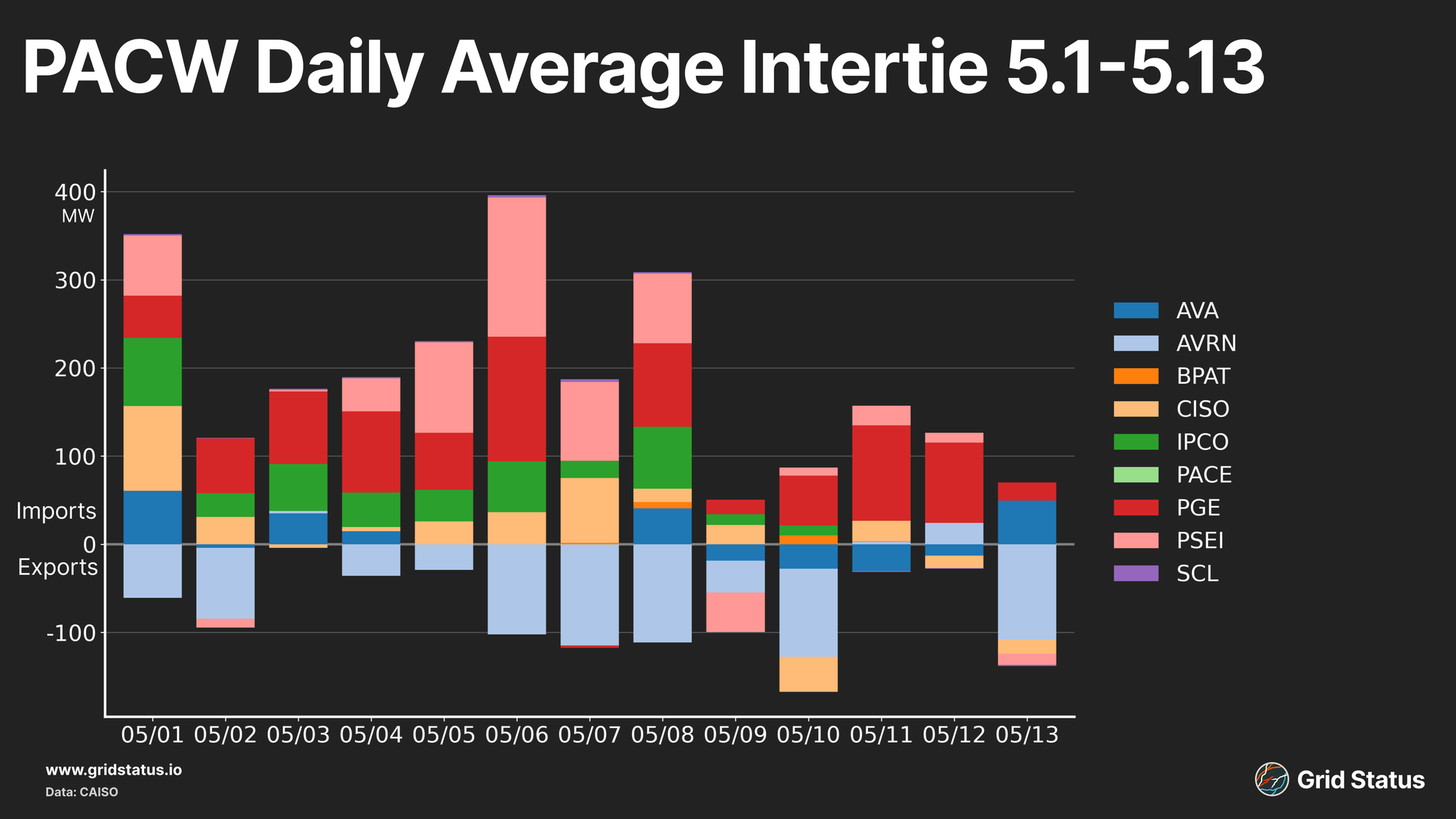

PACW is a net importer as net generation tracks below load, namely from nearby Portland General Electric and Puget Sound Energy. PACW also got flows from CAISO early in the market life, but has recently seen exports. As temperatures rise in California and the PNW stays mild, PACW transfers power from surrounding BA’s into California to help aid in their peaking load season.

PACE interchange sees increased variability, which is likely impacted by wind generation both located locally in the Balancing Authority and wind generation in surrounding BA’s. When wind generation is strong, the region has more excess MWs to send to the surrounding regions.

If you look really close at this chart, you will notice PACE interties from the CAISO fuel mix are missing our renewed friends in the west, SPP’s Western Market Entity, SWPW.

The Showdown: When West meets West

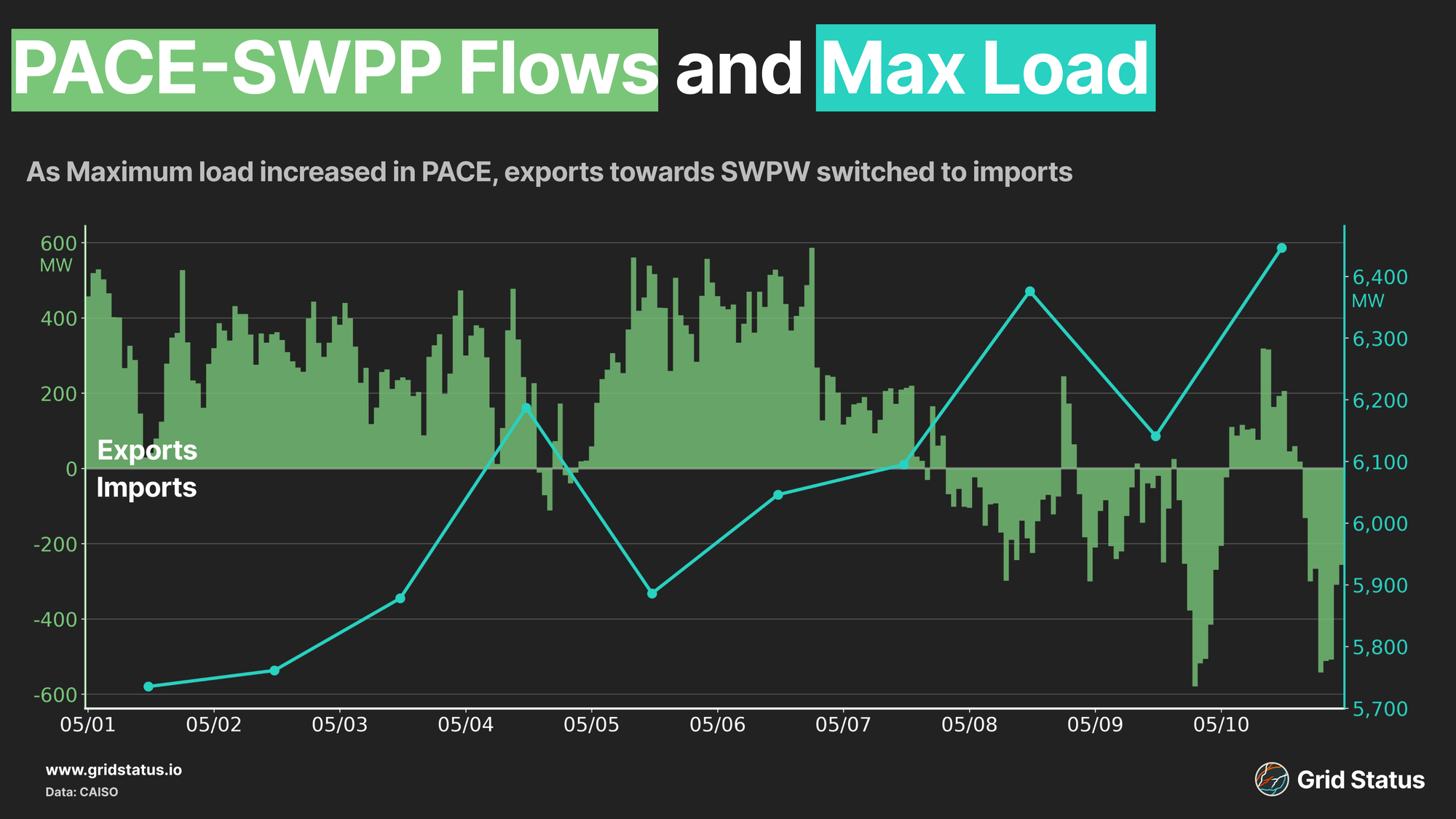

As we alluded to earlier, EDAM is not the only market change taking place in the neighborhood. PACE is also interacting with a new day-ahead market of SPP on its eastern side, which is part of a fulsome RTO expansion in its own right, and not just the day-ahead market. Expanding across the HVDC tie line just a month before EDAM’s go-live, two regions are now both operating in a Day-Ahead market, so let’s take a look at how they are interacting.

SPP West is a net importer from its surrounding regions, including PACE. Just after go-live, PACE consistently exported to SWPW. After this first week flows flipped, with SPP West now exporting to PACE.

This switch appears to be driven by an increase in load in PACE, as the peak increased, the flows inverted.

Despite the higher level of wind and solar compared to its Western half, PACE has a high level of thermal generation, namely coal. Solar generation drops heading into the load peak, leading to the need for dispatchable generation. SWPW is a net importer, but has a wealth of surrounding BA’s in the west that it obtains flows from, which are subsequently likely supporting PACE as temperatures rise.

Can We Get a Replay: Unusual Activity

The first few days of EDAM saw Day Ahead price clears follow expectations: prices largely tracked net load, with the highest prices during the evening peak.

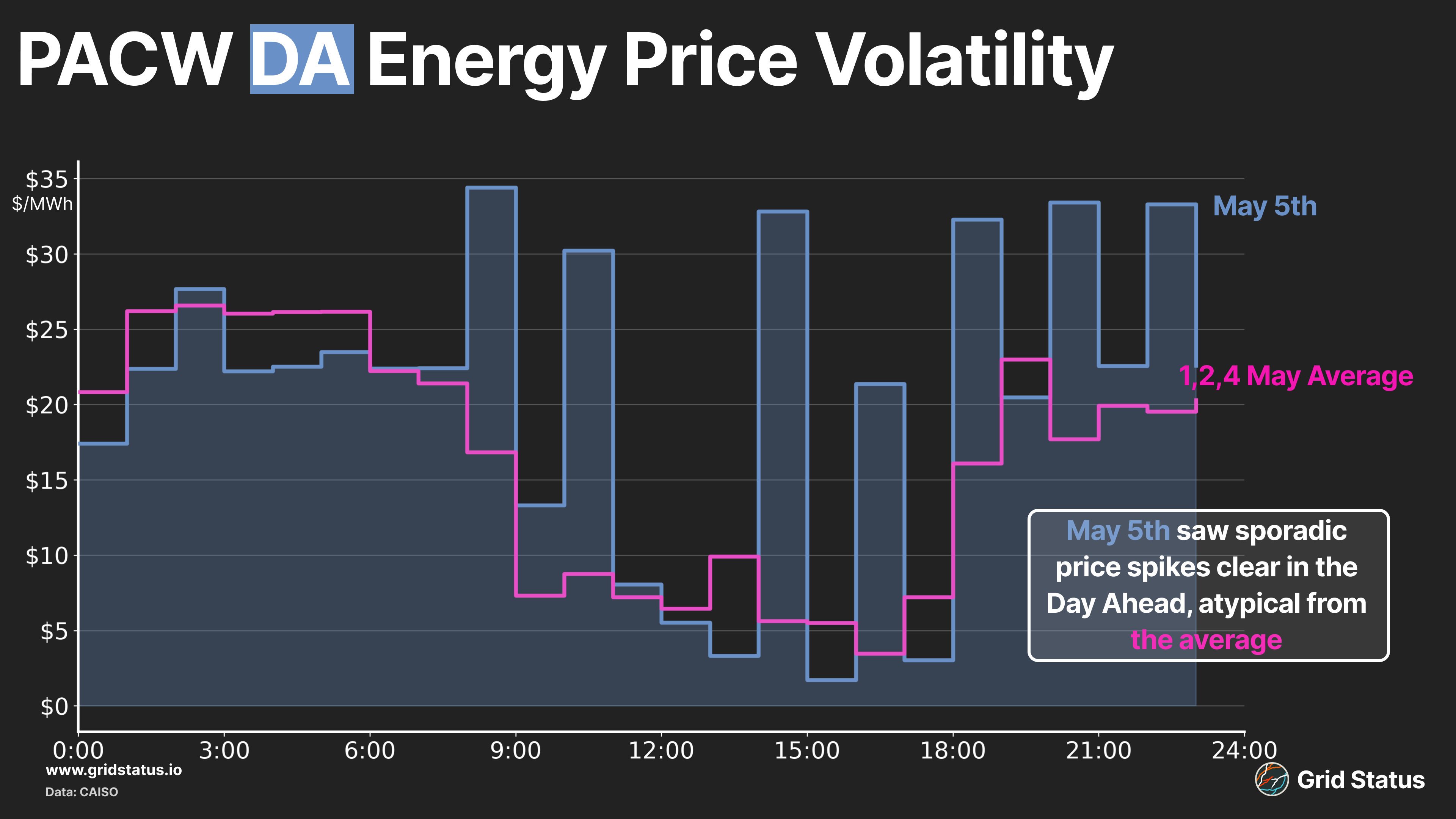

However, on May 3rd, the PACW DA clear displayed peculiar volatility throughout the mid-day. Real-time prices tracked what would be thought of as ‘typical’, showing a smooth curve as expected from market fundamentals. This volatile price clear occured again on May 5th, but this time, real-time prices tracked above the clear.

PACW day-ahead prices have been relatively smooth since, and while a direct cause isn’t obvious, it implies a relatively thin bid stack on this day. PACW is a small balancing authority in the grand scheme of things, barely breaching 2.5 GW peak load recently and with only ~2.7 GW of internal generation, of which perhaps a third isn’t dispatchable. Under those conditions and with a new market to find footing in, it doesn’t take much to obtain a spikier day-ahead clear.

The mind does jump to dispatchable gas, and PACW does contain a single 1990s combined-cycle unit at Hermiston (predating any carbon pricing in Oregon), but it would be tough to reach prices in the +$30/MWh range right now. Gas at KingsGate on this day was ~$1, and this plant averaged an 8.4 heat rate in 2025. With that price and efficiency, variable O&M would have to be far beyond typical values to get even close to that $30 range.

Congestion Contention

We’ve previously covered friction over allocation of congestion in EDAM, but in a recent report, CAISO’s Department of Market Monitoring identified the (interim) cure as possibly worse than the original affliction itself.

Quoting directly from the DMM’s recent report:

. . .one of the chief problems with the interim CRA is that it creates incentives to self-schedule energy to receive CRA payments rather than submit price sensitive bids. Such self-scheduling is inefficient on its own and could also increase congestion prices, thereby increasing the incentive for others to self-schedule. Additional self-scheduling could further increase congestion prices and potentially start a vicious circle resulting in severe market dysfunction and—in worst case scenarios—the collapse of price sensitive bid submissions to the market.

CRA in the above stands for Congestion Revenue Allocation. Under the currently active interim EDAM CRA, the incentive to self-schedule comes from the ability of firm transmission scheduling rights holders to receive CRA payments from a receiving area, but requires the rights holder to have self-scheduled energy in the EDAM.

In the report linked above, the DMM estimated which schedules could have been profitable to self-schedule under the interim CRA using historical WEIM data. Their findings suggest that the CRA as is would incentivize the feared self-scheduling, and that while it may not be a major issue with a smaller pool of early participants, the issue would “grow significantly” as new BAAs join the market. With the start warning delivered in this report and ongoing attention from previous publications, interest in the “correct” form of CRA will remain at the heart of EDAM market design going forward.

Something in the Air: Greenhouse Gas Pricing

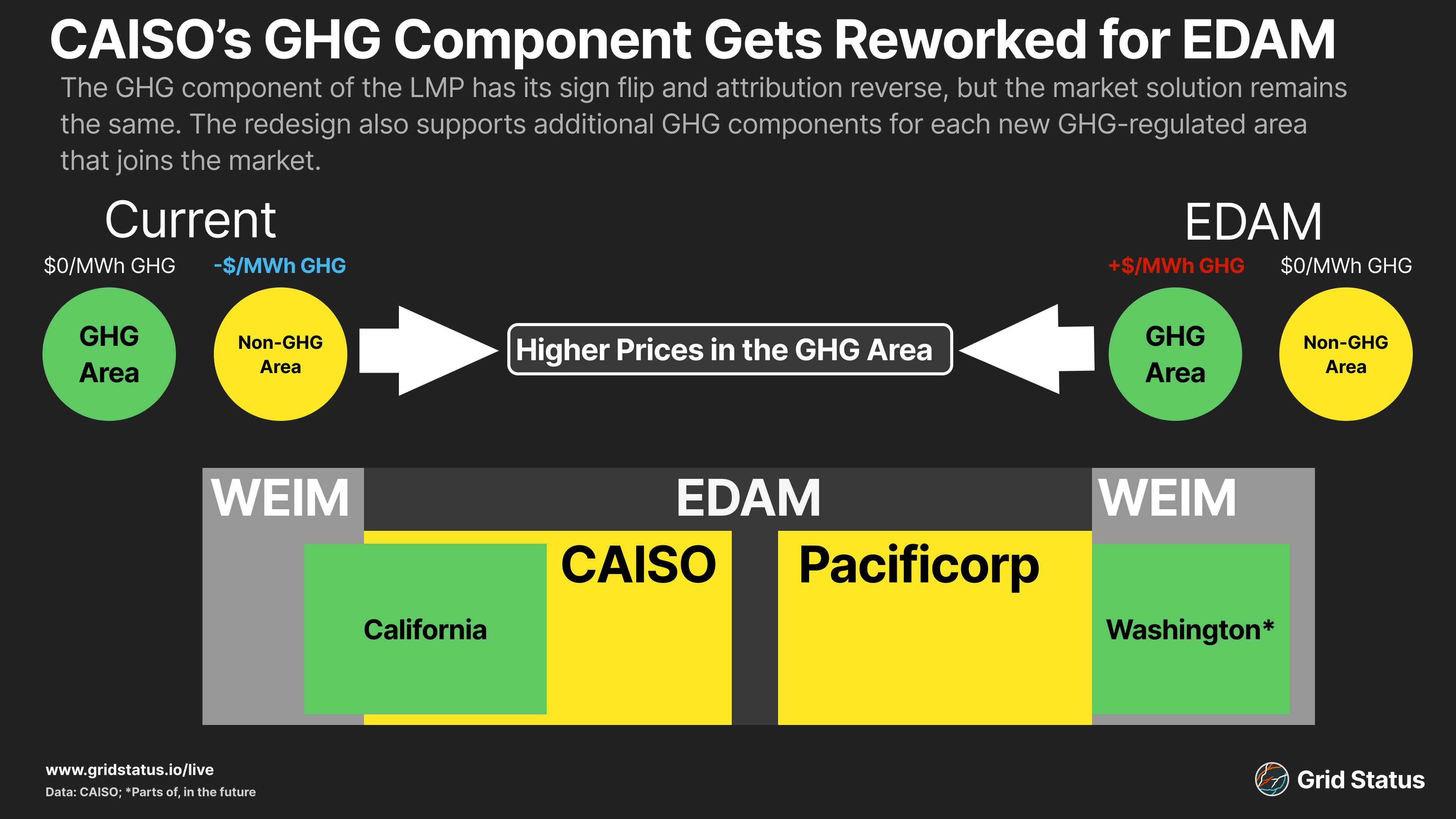

When it comes to the GHG component under EDAM, CAISO is taking notes from the East Coast, to flip it and reverse it by applying a positive GHG LMP component (MC-GHG) to GHG-regulated areas instead of the current negative LMP component applied to non-GHG areas.

In this context (and plenty of others in market design), it's useful to internalize that a higher internal price is functionally equivalent to a lower external price. The sign change doesn't alter solutions and won't have an effect on market outcomes, which CAISO's GHG Price Formation materials emphasize.

One of the key market changes that made this switch possible is the separate Marginal Energy Components (MECs) between different areas, e.g., Pacificorp and CAISO will have different MEC values in their LMPs (the same way SPP East and West now have different energy components).

At EDAM's launch (with limited participation), there are some basic scenarios with easy-to-understand outcomes in terms of GHG prices:

- California GHG-Area is net exporting = $0/MWh GHG Price;

- Pacificorp Non-GHG-Area is net importing = Internal resources cannot serve the California GHG-Area;

- No transfer into CAISO from PACW/PACE = Difference between CA-GHG marginal resource bid and CAISO MEC (which can be set by a resource in the non-GHG area) is the GHG price.

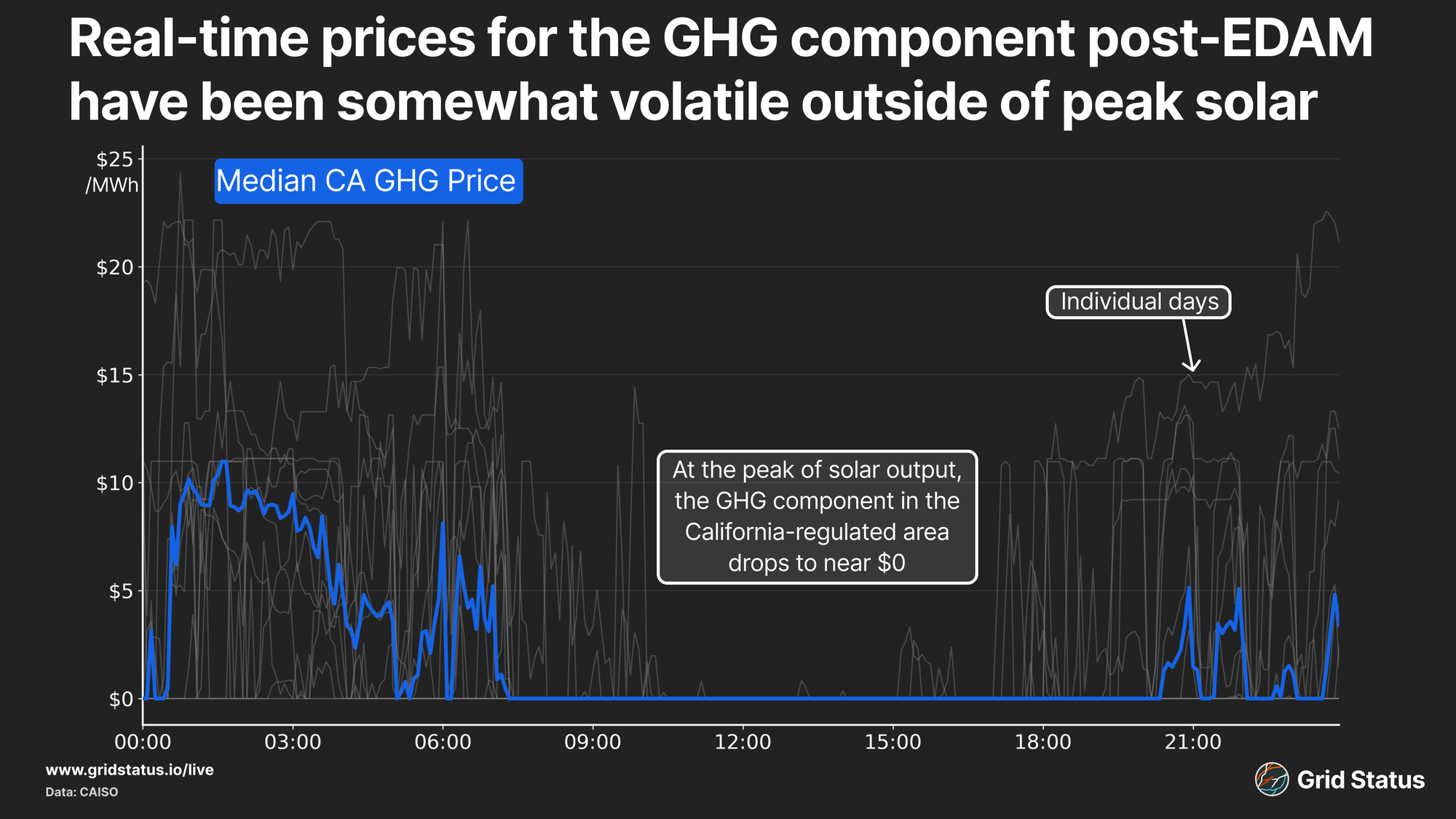

In terms of outcomes so far, the GHG component has tended towards $0/MWh during peak solar output hours (when the CA-GHG-regulated portion of CAISO is most oversupplied), with a decent amount of volatility outside of those hours, particularly overnight and close to sunrise.

Day-ahead prices have displayed largely the same pattern. We have a limited number of days to track this so far, and the net export constraint for GHG transfers was unable to make the market’s launch, so at least one design element has yet to be implemented. As we move through the summer into higher-demand periods, it will be interesting to track this price and what offers are made to serve the CA-GHG area from other balancing authorities.

GHG Terms to Know:

MC-GHG - Marginal Cost of Greenhouse Gas, a component of the LMP in CAISO-administered power markets. The shadow price to serve a a GHG-regulated area instead of a non-regulated GHG area. Per CAISO: “the MC-GHG generates revenue funded by load in the GHG area which is used to cover costs outside the GHG area when the least-cost solution for the GHG and non-GHG areas diverge”

Secondary Dispatch - Lower-emitting resources outside of a GHG-regulation zone receive dispatch signals for the GHG zone, which leaves higher-emitting resources to backfill in the non-regulation area in place of the lower-emitting resources.

GHG Reference Pass - A counterfactual run in the Integrated Forward Market (IFM), which generates a market schedule without GHG-area net imports. This simulates how non-GHG areas would meet internal load and provide external supply in the absence of GHG-area demand. This counterfactual serves as the baseline to limit GHG transfer attribution to the difference between a resource's reference schedule and upper economic limit. Specifically, the IFM:

“would limit an attribution to the lower of: (1) the GHG bid capacity; (2) the positive difference between a resource’s upper economic limit and its GHG reference pass; or (3) the optimal energy schedule.

In real-time, CAISO would rely on the EDAM resource’s day-ahead schedule to limit the MW value of a real-time GHG transfer, the lower of: (1) the MW value of the GHG bid adder; (2) the resource’s upper economic bid minus day-ahead energy schedule, plus the resource’s total day-ahead attribution to serve in”

GHG Net Export Constraint - GHG transfers from EDAM resources in non-GHG areas can't exceed the net exports of that area. Simply put, if the BAA is a net importer for a given hour, no internal resources can serve GHG-regulated load in the same hour. This mechanism is meant to reduce Secondary Dispatch along with the GHG Reference Pass. The GHG Net Export Constraint has an exception that allows relaxation of the constraint for reliability risk situations.

GHG Area - Not CAISO! This might trip folks up given the relationship between CAISO and the state of California, but CAISO itself is not a GHG-area. Not all of California is in CAISO, and not all of CAISO is in California. Valley Electric Association (VEA), which is located in Nevada and joined CAISO over a decade ago, is not subject to the same greenhouse gas regulations as the California portions of CAISO.

DAME Brings Reliable Balance to the Grid

EDAM wasn’t the only big change, as its anagram-sister, DAME (day-ahead market enhancements), also went live on May 1st. With its launch, DAME brought two new market products: Imbalance Reserve and Reliability Capacity (both up and down variants). Previously, day-ahead awards covered energy and ancillary services; now, Imbalance Reserves and Reliability Capacity have been added as independent elements.

One aspect of IR and RC that may surprise those not deep into CAISO processes is the fact that their prices are neither system-wide, nor EDAM-area or regionally-based.

Rather, individual nodes receive prices as the modeling of these products is closer to LMPs than the bulk procurement typically seen with traditional ancillary services.

Imbalance reserves (IR) are procured in the Integrated Forward Market (IFM), part of the day-ahead process, with the goal of having enough bid-in capacity to handle inherent uncertainty between day-ahead and real-time for each EDAM participant. Each area procures IR on an hourly basis, co-optimized with energy and ancillary services, with requirements derived from forecasts for the next day as well as a combination of historical uncertainty in load, solar, and wind forecasts.

The BPM-stated purposes are:

- Up: Incremental capacity procured relative to the net load forecast to meet the upward uncertainty requirement

- Down: Decremental capacity procured relative to the net load forecast to meet the downward uncertainty requirement

The overarching goal of IR is to handle the net load imbalances and ramping requirements that appear between the day-ahead and real-time markets. As the penetration of weather-dependent resources has grown across the Western Interconnection, the disconnect between day-ahead outcomes and real-time forecasts has only grown. IFM awards carry a 15-minute dispatchable physical resource requirement, and awards are based on 15-minute ramp capability.

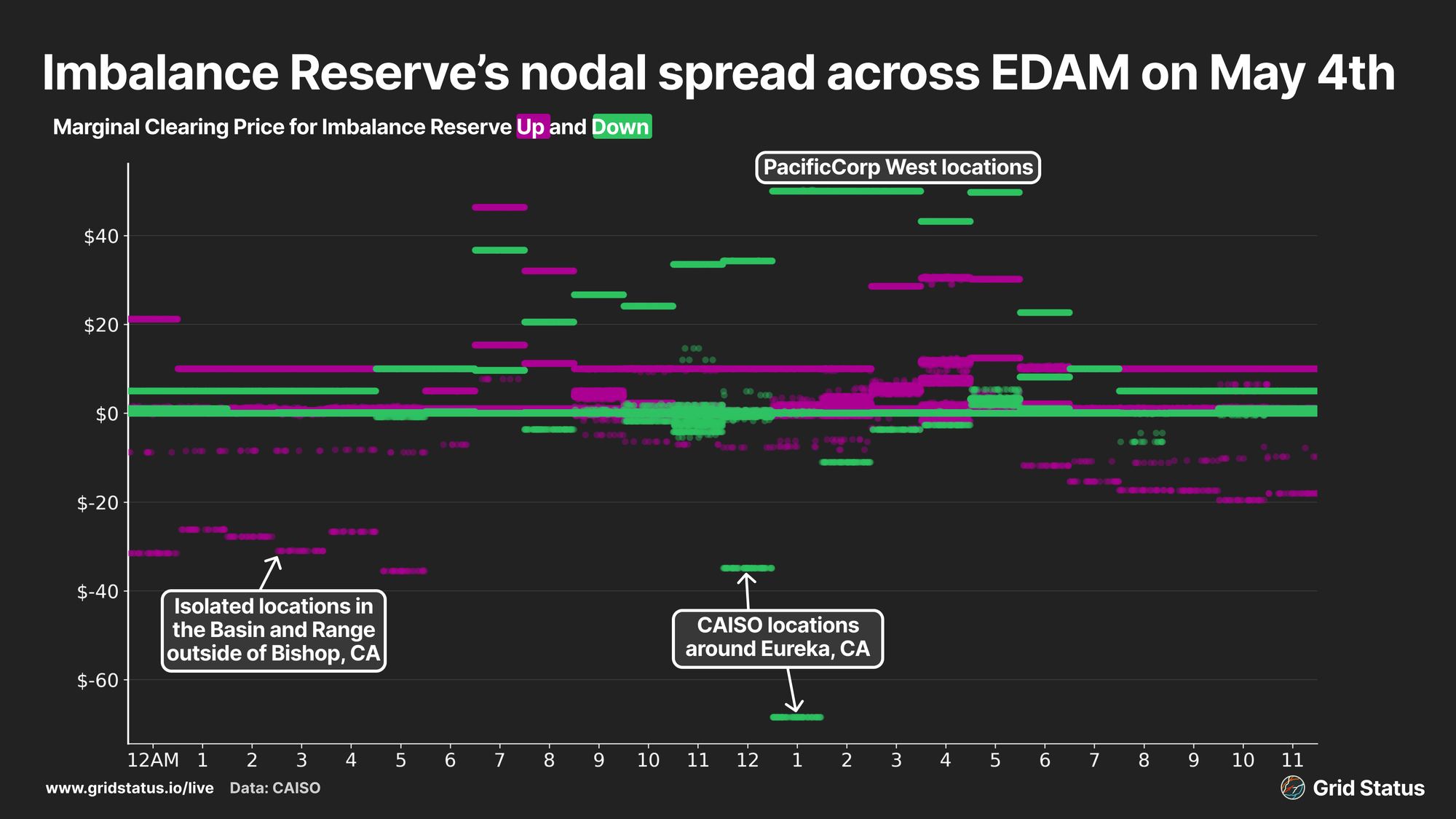

May 4th saw the largest spread across locations for both up and down variants of IR. PacificCorp West locations had the highest prices in the afternoon for the Down side of IR, while geographically-isolated nodes in CAISO had the lowest Up prices all day, demonstrating their inability to provide support to the wider system.

Reliability Capacity (RC) is also procured in the day-ahead, but as part of the Residual Unit Commitment (RUC) process. RUC is the final step in CAISO’s day-ahead process, occurring after the IFM. At a high level, IR is procured as part of the economic clearing process for tomorrow’s operations, while RUC is concerned with committing or making available additional reliability-driven capacity.

As with IR, each EDAM area procures RC on an hourly basis, but RC is not co-optimized with energy and ancillary services, which would have been previously procured earlier in the day-ahead process cycle. RC Up is for periods in which the forecast outstrips physical supply, while RC Down covers the inverse.

The BPM-stated purposes are:

- Up: Incremental capacity procured to meet the positive difference between the net load forecast and the cleared non-VER physical supply.

- Down: Decremental capacity procured relative to the net load forecast to meet the downward uncertainty requirement

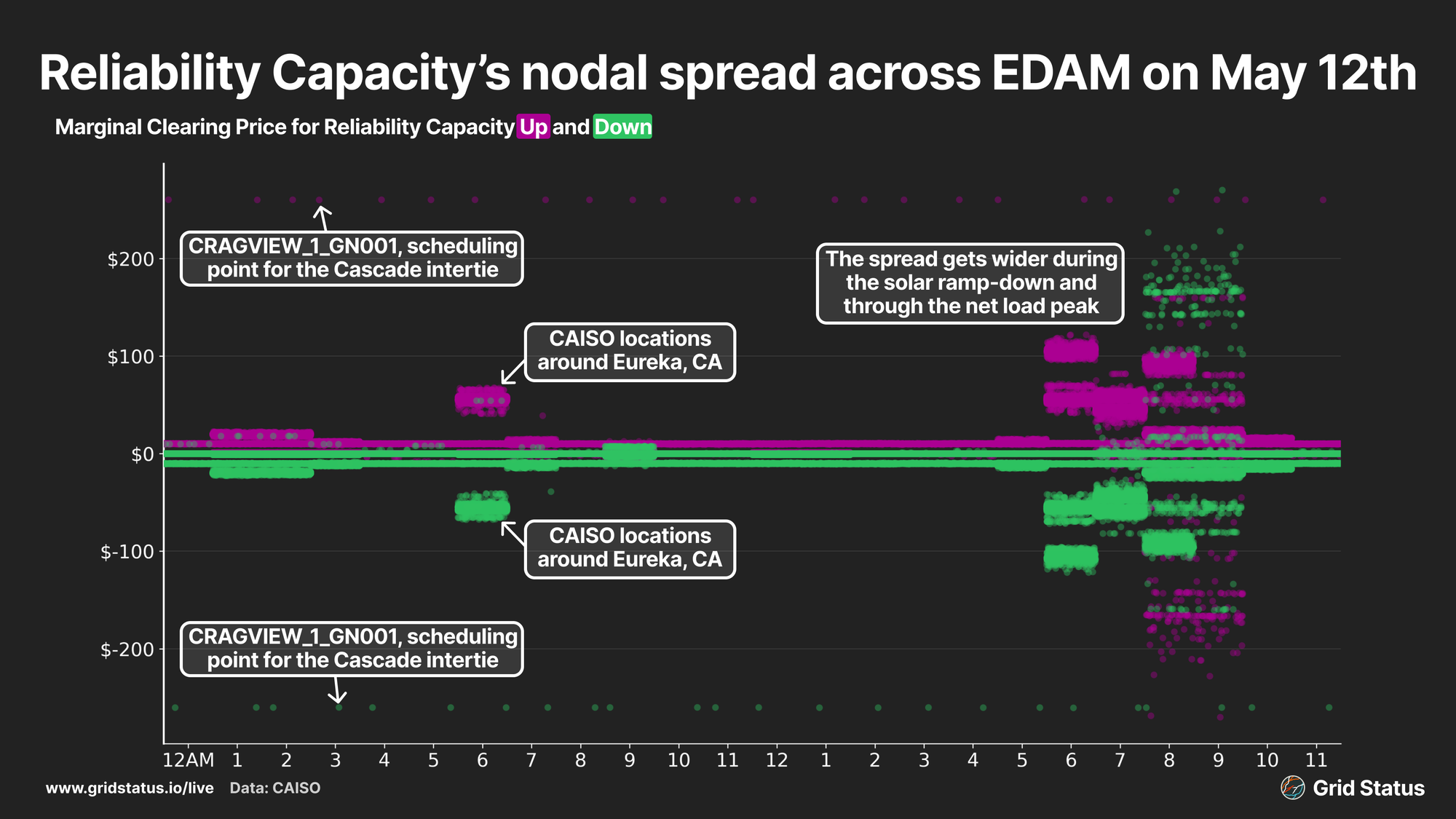

For RC, May 12th has had the widest spreads across locations. Unlike IR, however, RC Up and Down create a price mirror at each location as the sign is (somewhat intuitively) reversed in the calculation for each direction.

May 12th is also an excellent example of the intent with RC, handling procurement of capacity to manage uncertainty associated with the net laid forecast and non-VER capacity commitment. This is shown in the expansion of prices across locations leading into the solar ramp down and through the net load peak, hours 18 through 21.

These new products come with the typical real-time must offer obligation (RT MOO) attached to day-ahead commitments, and if the scheduling coordinator fails to submit bids in real time, the market automatically inserts bids matching the obligation. IR and RC do have a wrinkle to their MOO that separates them from traditional ancillary services: their real-time energy bids must be economic, while MOOs derived from ancillary services can be economic or self-schedule.

The Next Mile: What’s Next for EDAM

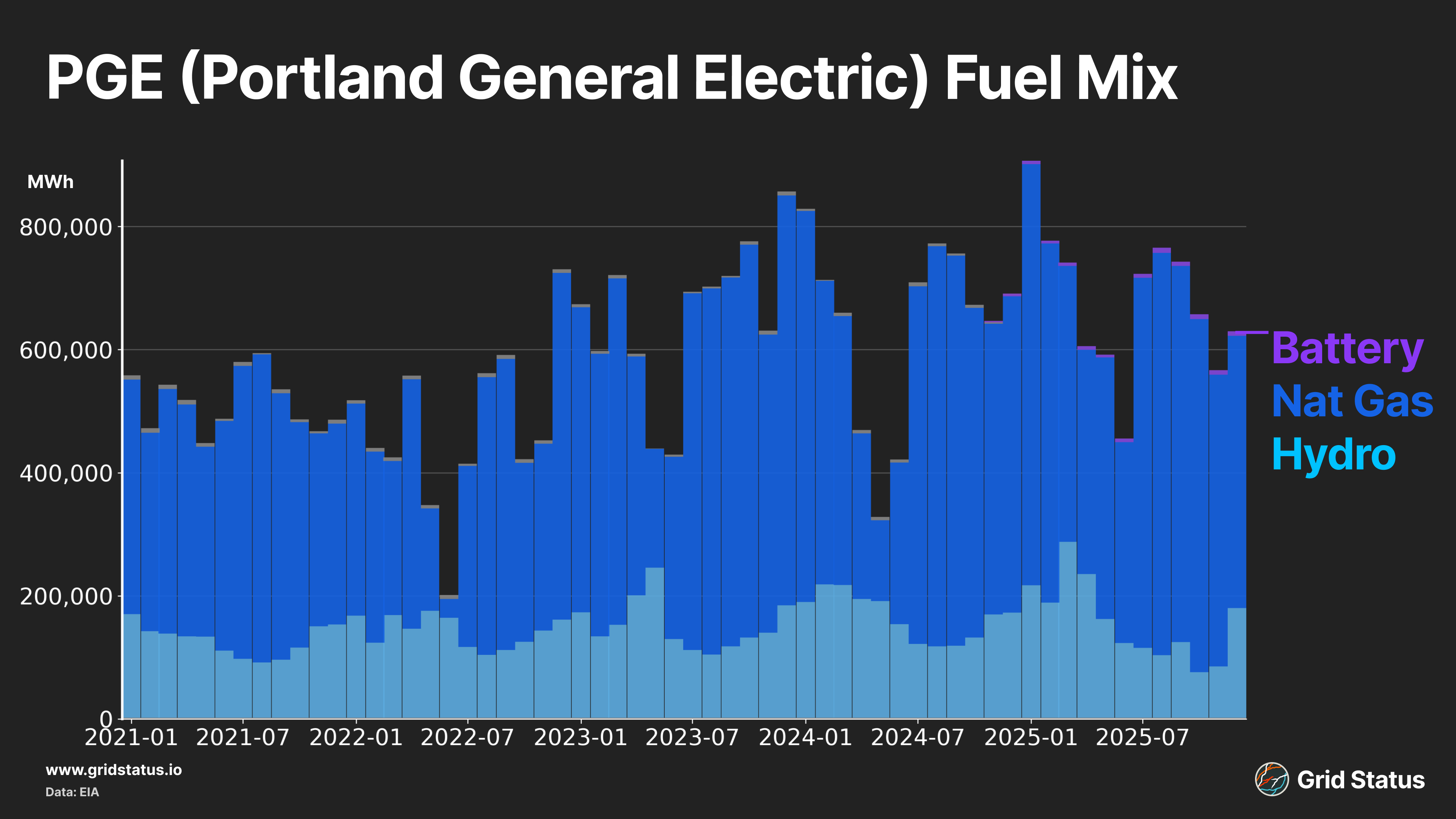

Portland General Electric is scheduled to join EDAM in October 2026. Another Pacific Northwest entity that neighbors PACW, the fuel mix comprises mostly of natural gas and hydropower with an increasing battery element. PGE also imports between 1-2.5 GW from Bonneville Power Administration (BPA) during the day as BPA remains in control of transmission lines for PGE assets.

Earlier this year, PGE announced that it is buying the Washington State portion of Pacificorp. The acquisition includes the following facilities in Washington state: Chehalis, a 600 MW natural gas plant, Marengo, a 234 MW wind plant, and Goodnoe Hills, a 100 MW wind plant. It is interesting to see ownership of assets change just as these BA's are moving into a combined market with closer operational coordination.

PGE’s fuel stack with this purchase will become more renewable-focused. Additionally, the addition of these assets should increase flows from PGE to PACW.

In 2027, EDAM will continue to expand, but this time outside of the Pacific Northwest. Non-CAISO balancing authorities inside the state of California planning to join LA Water and Power, Turlock Irrigation District, and Balancing Area of Northern California. Additionally, the Public Service Company of New Mexico is targeting 2027. This wind and solar-heavy BA located in the Desert Southwest will provide an interesting dynamic as it is less directly connected to CAISO. Lacking sufficient baseload power, this region relies on imports when renewable generation dies down.

While the start of this new Market is certainly exciting to analyze and watch, things are only going to get more interesting in the following years as more and more balancing authorities join EDAM. We also have one more market coming into the fold, SPP’s Markets+, a competing Day-Ahead concept from the now dual-interconnection RTO, which has secured commitments from several major balancing authorities across the west.